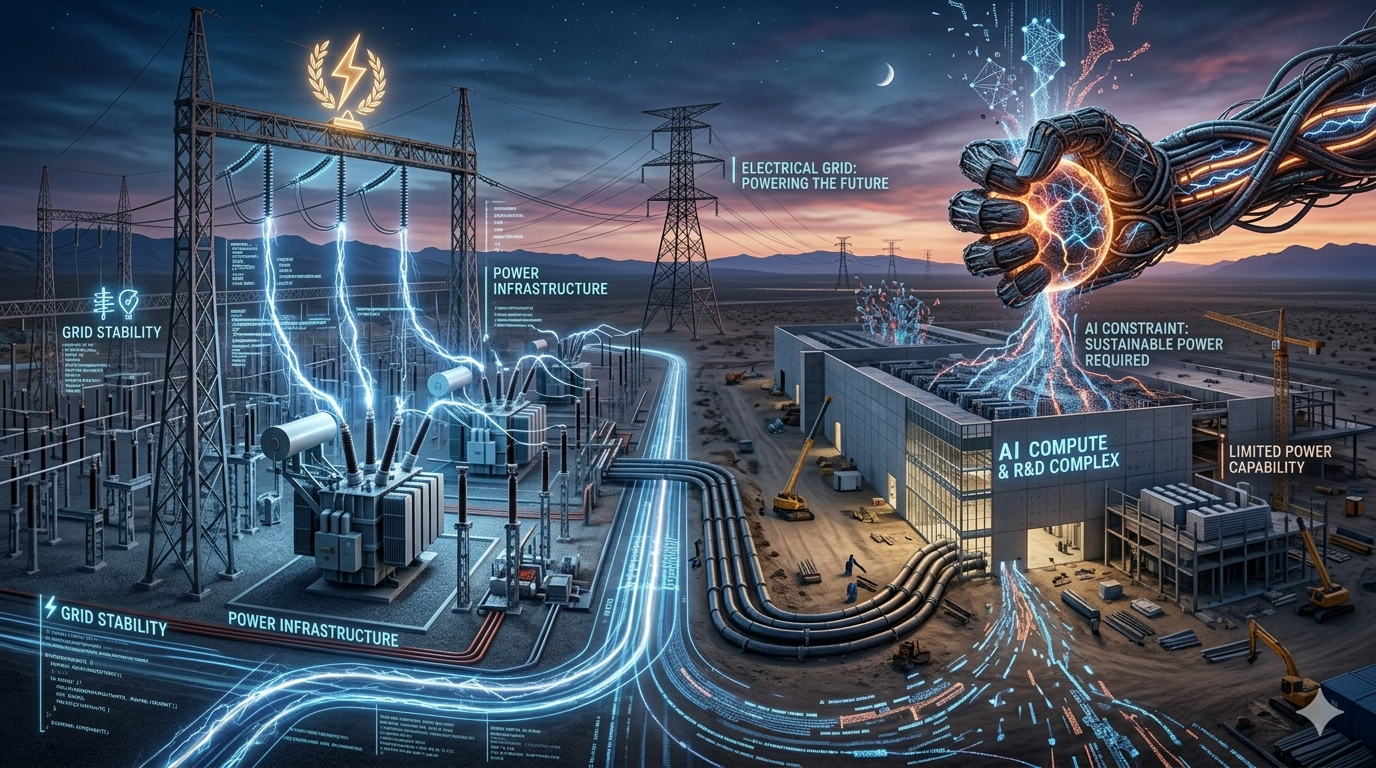

The AI Industry Has Found Its Next Constraint

For most of the past three years, the artificial intelligence industry focused on one question: who could build the most capable model?

The conversation revolved around graphics processing units, training clusters, model parameters, and semiconductor supply chains. Every major announcement highlighted larger models, faster chips, and expanding compute capacity. Consequently, investors, policymakers, and technology leaders viewed semiconductors as the defining resource of the AI era. That narrative is beginning to change. Across global markets, a different constraint is emerging. The challenge no longer centers solely on obtaining advanced processors. Instead, it increasingly involves securing enough electricity to power them.

As AI adoption accelerates, power availability is becoming a strategic differentiator. Data center operators are evaluating energy access before selecting locations. Utilities are entering conversations that once belonged exclusively to cloud providers and technology companies. Moreover, grid capacity is influencing expansion plans for some of the world’s largest AI infrastructure projects. The AI race is no longer confined to software development. Increasingly, it is becoming an infrastructure story.

Why Electricity Has Become the New Scarce Resource

The AI ecosystem consumes power at a scale that traditional digital workloads rarely required. Training large language models demands enormous computational resources. Inference workloads, meanwhile, operate continuously and require sustained energy consumption. As organizations deploy AI services to millions of users, demand for electricity grows alongside demand for compute. This shift creates a fundamental challenge. Semiconductor manufacturing can expand through additional investment and production capacity. Electricity infrastructure, however, cannot scale overnight. New transmission lines, substations, generation facilities, and grid upgrades often require years of planning and construction.

As a result, access to power is becoming a limiting factor. Several data center markets already face delays linked to grid constraints. Developers increasingly evaluate available megawatts before evaluating real estate opportunities. In some regions, power access has become more valuable than land availability. This development marks a significant change in how the technology industry approaches growth. For decades, software companies operated largely independent of energy discussions. Today, electricity planning is becoming part of technology strategy.

Utilities Are Becoming Strategic Technology Partners

The transformation creates an unexpected winner. Utilities have traditionally occupied the background of the digital economy. They supplied power while technology companies built applications, platforms, and services. AI is changing that relationship. Power providers are increasingly participating in strategic discussions surrounding data center expansion. Utility companies now influence project timelines, infrastructure investments, and regional competitiveness. Their role is expanding because AI facilities require unprecedented energy density.

Modern AI clusters consume significantly more electricity than traditional enterprise environments. High-performance computing environments, accelerated workloads, and large-scale inference operations place substantial demands on local grids. Consequently, utilities are evolving from service providers into critical ecosystem partners. The development reflects a broader shift within the infrastructure landscape. Technology companies may continue designing advanced AI systems, but utilities increasingly determine where those systems can operate at scale.

Data Center Site Selection Is Being Rewritten

Historically, data center location decisions emphasized connectivity, tax incentives, and real estate economics. Those factors remain important. However, power availability is moving to the top of the decision-making process. A region with abundant fiber connectivity but limited grid capacity may struggle to attract future AI investments. Conversely, locations with reliable energy infrastructure may become highly desirable despite higher operational costs. This change has significant implications for global infrastructure development.

Regions that invested in transmission networks, renewable energy projects, and grid modernization may find themselves better positioned for the next wave of AI expansion. Meanwhile, markets facing energy shortages could encounter growing challenges in attracting large-scale deployments. The result is a new competitive framework. Data center growth increasingly depends on energy readiness rather than simply digital readiness.

The Rise of Energy-Centric AI Economics

The financial implications extend beyond infrastructure planning. Electricity costs now influence the economics of AI deployment. As organizations scale AI services, energy expenses become a larger component of operational expenditure. This trend introduces a new layer of complexity for technology leaders. Model efficiency remains important. Hardware optimization remains essential. Yet the economics of AI increasingly depend on the ability to access affordable and reliable power.

Investors are beginning to recognize this reality. The market has devoted substantial attention to chip manufacturers, cloud providers, and AI startups. However, the long-term value chain may extend further into the energy sector than many anticipated. Utilities, transmission operators, and power infrastructure developers could become increasingly important participants in the AI economy. That possibility challenges traditional assumptions about where value creation occurs within the technology ecosystem.

The Next AI Leaders May Be Energy Leaders

The industry continues to celebrate breakthroughs in reasoning, multimodal capabilities, and agentic systems. Those advancements matter. However, the infrastructure supporting AI deserves equal attention. Every new model requires compute. Every compute cluster requires electricity. Every expansion plan ultimately depends on access to power. This reality suggests a broader conclusion. The next phase of AI competition may not be determined exclusively by software innovation. It may also be shaped by energy strategy, grid modernization, and infrastructure investment. Technology companies are unlikely to stop pursuing more powerful models. Nevertheless, the organizations that secure reliable energy access could gain a significant advantage as AI adoption accelerates. The AI industry spent years focusing on silicon. The next decade may belong to the electric grid.

The Commentary

The technology sector often searches for disruption in the wrong places. Today, much of the attention remains fixed on model releases and semiconductor roadmaps. Yet the more consequential shift may be happening outside data centers and beyond AI laboratories. Electricity is emerging as the foundation upon which future AI growth depends. That development does not diminish the importance of software innovation. Instead, it highlights an uncomfortable reality. Intelligence at scale requires infrastructure at scale. As AI moves from experimentation to economic necessity, access to power may become one of the defining competitive advantages of the digital era. The companies building the future of AI still need advanced chips. Increasingly, however, they need something even harder to secure.