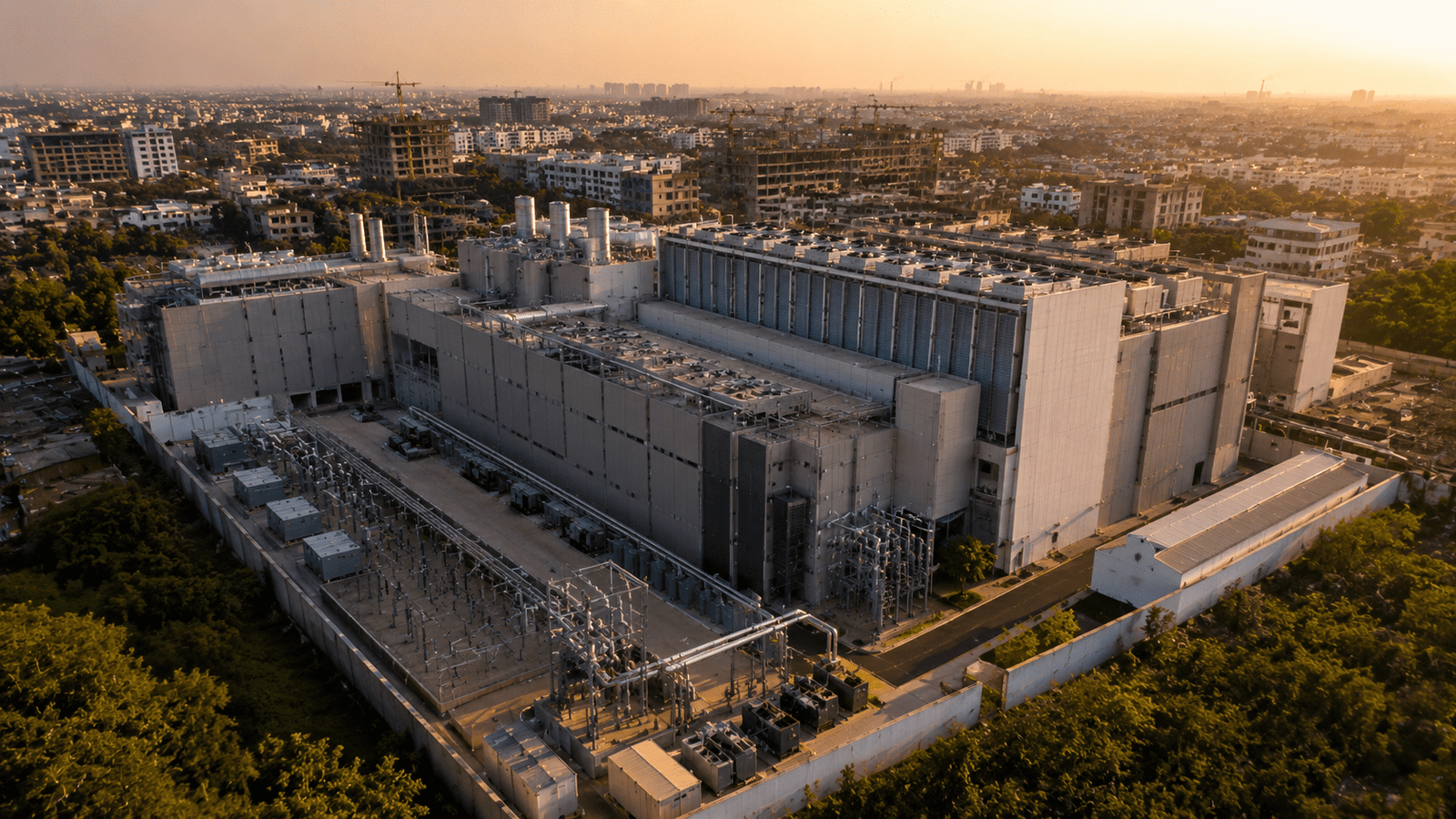

India’s data center market has spent the better part of a decade being talked about in terms of Mumbai, Chennai, Hyderabad, and Bengaluru. Those four cities have, for good reason, dominated the conversation. They have the connectivity, the enterprise customer base, the skilled workforce, and the established developer relationships that make large-scale data center investment straightforward to justify. The next chapter of India’s data center story is, however, not being written in those markets. It is being written in Pune, Ahmedabad, Vizag, and Kochi. A growing list of cities that were, until recently, not part of any serious data center conversation is, in turn, expanding.

That shift is not accidental. It is the product of specific structural pressures making Tier 1 markets increasingly difficult to develop at scale. Those same pressures are, in turn, making Tier 2 markets increasingly attractive for the infrastructure that Indian AI demand will require next. Understanding why requires looking at what those pressures actually are, and what the developers and hyperscalers responding to them are, specifically, betting on.

What Is Making Tier 1 Markets Harder

The Tier 1 data center markets in India face a set of constraints that are, notably, familiar to anyone watching the same dynamic play out in Western markets. Land availability in Mumbai’s primary data center corridors is increasingly scarce and increasingly expensive. Power availability in Hyderabad is running into grid capacity constraints. The city has seen some of the fastest data center growth in India over the past three years. State utilities are working to address the constraint but cannot resolve it quickly. Chennai faces similar land and power pressures. Water availability concerns are, additionally, particularly acute for data center cooling in a coastal market with periodic water stress.

The connectivity argument for Tier 1 cities is also, specifically, weakening. India’s national fiber backbone has improved dramatically over the past five years. A Tier 2 city in 2026 can offer connectivity that would have been only available in a Tier 1 market in 2018. For workloads where latency is not the primary constraint, however, it substantially changes the calculus. Power cost is, however, the most decisive factor. Industrial power tariffs in several Tier 2 states are, in turn, materially lower than in the primary Tier 1 markets.

Andhra Pradesh has been actively courting data center investment with power pricing that reflects its surplus generation capacity. Its significant renewable energy ambition is, notably, driving that surplus. Rajasthan is, similarly, offering power at rates that make data center operating economics considerably more attractive than in Maharashtra or Karnataka. Its large-scale solar deployment is the structural reason why. That cost differential compounds over the life of a data center asset. A Tier 2 location becomes, consequently, genuinely competitive on total cost of ownership even when land and construction costs are factored in.

What Tier 2 Cities Actually Offer

The case for Tier 2 markets is not just about what Tier 1 markets lack. Several Tier 2 cities are, notably, building specific advantages that go beyond cost arbitrage. Pune is the most developed example. Pune sits close enough to Mumbai to share connectivity infrastructure and enterprise customer proximity. Land costs are, however, substantially lower and power availability is less constrained. Several major operators have already committed to Pune capacity. The market is, consequently, developing the ecosystem of contractors, skilled workers, and support infrastructure that makes further investment easier to justify.

Kochi is, specifically, positioning itself as a submarine cable landing point alternative. That gives it genuine connectivity advantages for traffic originating in the Middle East and Southeast Asia. The CODA and 2Africa cable systems both have landing points in India. Markets with physical proximity to those landing stations hold connectivity advantages that inland locations cannot, notably, replicate. Vizag, similarly, has both submarine cable access and a state government that has been aggressive in offering incentives and fast-tracking approvals for data center development.

State government support, lower land costs, and proximity to a large industrial economy that generates genuine data demand all converge in Ahmedabad. It is, specifically, one of the most interesting Tier 2 data center markets in India right now. Gujarat’s industrial policy has been consistently more business-friendly than most Indian states. Its track record on infrastructure delivery has, in turn, made it a credible destination for capital that requires reliable execution.

What the Developer Bets Reveal

The developers moving first into Tier 2 markets are, notably, not doing so because Tier 1 markets are saturated. Tier 1 markets still have significant committed pipelines and active development. They are moving because the risk-reward calculation for Tier 2 markets has, in turn, shifted materially in the past two years. Land banking in Tier 2 markets is considerably cheaper than in Tier 1. The cost of being wrong about a Tier 2 bet is, consequently, lower. The cost of being right is, however, potentially very high if those markets develop into major data center destinations over the next five to ten years.

The hyperscaler behaviour is, also, the most instructive signal. Google‘s commitment to data center infrastructure in India has not been concentrated exclusively in Tier 1 markets. Microsoft‘s Azure expansion has similarly covered markets beyond the traditional four. When hyperscalers start building in a market, the co-location operators, network providers, and power infrastructure companies follow. That sequencing is, in turn, beginning to play out in several Tier 2 markets. The current wave of Tier 2 investment is, specifically, not speculative. It is, rather, the early phase of a structural reorientation of Indian data center geography. That reorientation will, ultimately, reshape where the country’s digital infrastructure is built over the next decade.