Three years ago, India was a data center market that global operators watched with interest and invested in cautiously. The demand story was compelling but the execution environment was complex. Power constraints, permitting delays, and a limited ecosystem of specialist contractors made large-scale development slower and more expensive than the headline investment numbers implied. That environment has not disappeared. However, something has shifted in the scale and conviction of capital flowing into Indian data center infrastructure that has moved the market from a cautious growth story into one of the most active construction pipelines in the world.

India’s data center colocation market is growing 25.5% annually and will reach $7.31 billion in 2026, with the broader data center market on track to reach $22 billion by 2030 from approximately $10 billion in 2025. The $60 to $70 billion in announced investments over the next five years, primarily from hyperscale operators and joint venture platforms, represents a structural commitment rather than speculative positioning.

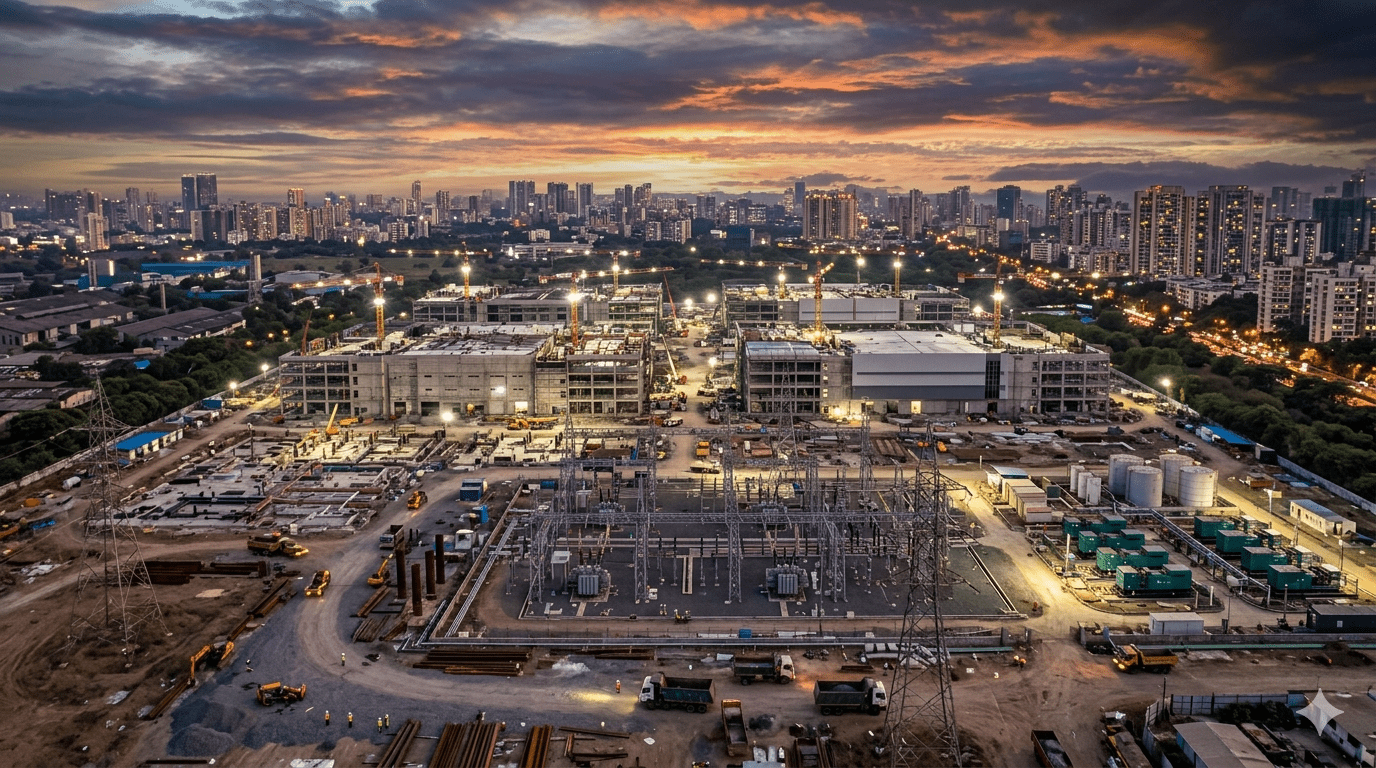

The capacity numbers tell the same story. India’s operational data center capacity currently stands at approximately 1.4 to 1.6 gigawatts across 164 facilities, with more than 700 megawatts under construction and a further 1 to 1.2 gigawatts in the planning stage. Installed capacity will rise to 1.7 to 2 gigawatts by the end of 2026 and expand to 4 to 5 gigawatts by 2030, backed by nearly $30 billion in cumulative investments, according to Vestian’s April 2026 report. Mumbai leads with approximately 41% of current national capacity, followed by Chennai at 23% and Delhi NCR at 14%. Additionally, Bengaluru and Hyderabad are emerging as significant secondary markets driven by renewable energy access and AI-focused campus development. The construction pipeline underway right now across these markets represents the largest sustained data center buildout India has seen and one of the largest in Asia-Pacific.

The GPU and Cloud Demand That Is Driving It

The IndiaAI Mission has allocated 34,000 GPUs for domestic AI development under its Compute Pillar, with officials confirming plans to scale to over 100,000 GPUs by end 2026 pending budget approvals and vendor deliveries. Yotta Data Services, which currently holds approximately 60 to 70% of India’s GPU capacity according to its own disclosures, is expanding its Shakti Cloud to 20,736 Nvidia Blackwell Ultra GPUs by August 2026. Reliance Jio, in partnership with Nvidia, is deploying GH200 Grace Hopper Superchips and DGX Cloud services to establish India’s first GPU-as-a-service cloud infrastructure at commercial scale. The combined public and private GPU expansion underway positions India to add meaningful sovereign AI compute capacity within a two to three year window, moving from a near-standing start to a regionally significant compute base.

India’s cloud market is growing at more than 20% compounded annually, driven by enterprise migration from on-premise servers to scalable cloud environments, 5G-driven data consumption growth, and the Digital Personal Data Protection Act’s data localisation requirements. The DPDP Act is expected to drive significant additional domestic data center demand by 2027 as multinational companies establish local infrastructure to comply with data residency mandates. Furthermore, average monthly wireless data consumption has crossed 25 gigabytes per user in India, creating sustained demand growth for the storage and compute infrastructure that underpins digital services at population scale. As covered in our analysis of India’s data center transmission problem, the constraint on converting this demand into operational capacity is not capital or intent but the power transmission and grid infrastructure required to support it.

What the Hyperscaler Commitments Actually Look Like

The scale of individual hyperscaler commitments to India in 2025 and 2026 has no precedent in the market’s history. Microsoft has committed $17.5 billion to AI and cloud infrastructure in India through 2029. Google confirmed a $15 billion partnership for cloud regions and AI data infrastructure, with its first AI-focused facility in Visakhapatnam, Andhra Pradesh developed in partnership with AdaniConneX and Airtel. Amazon Web Services expanded its Mumbai region by 40% and continues to add availability zones. These are not exploratory commitments. They are infrastructure programs with site selection complete, construction underway, and customer commitments attached.

Domestic operators are matching that energy with their own capital programs. AdaniConneX has set a target of 1 gigawatt of capacity backed by a $10 billion investment roadmap. Reliance Industries has announced a 3 gigawatt data center campus in Jamnagar, Gujarat, powered by renewable energy. CtrlS Datacenters has committed $2 billion for AI-ready green campuses. NTT DATA is developing a $1.2 billion AI cluster in Hyderabad. Together, the domestic and foreign operator pipeline targeting delivery by 2030 represents a capital commitment that, if executed at anywhere near its announced scale, will make India one of the five largest data center markets in the world by installed capacity. The execution challenge is real and significant. However, the direction of travel is not in doubt.

The Execution Gap That Could Limit the Upside

The honest assessment of India’s data center growth trajectory requires acknowledging the execution gap between announced investment and delivered capacity that has characterised previous cycles. Between 2020 and 2024, India attracted approximately $13 to $15 billion in data center investments, yet operational capacity grew more slowly than the investment volumes suggested it should. The reasons are consistent across projects: power availability constraints, permitting complexity at state and municipal levels, limited availability of specialist contractors for high-density liquid cooling installation, and grid interconnection timelines that stretch well beyond project construction timelines.

Those constraints have not been resolved. They are being managed more effectively than before, through behind-the-meter generation, renewable energy procurement, and state-level policy support that was not available in earlier cycles. However, the gap between the $60 to $70 billion in announced investments and the 3 to 4.5 gigawatt capacity projection for 2030 implies a capital efficiency per megawatt that requires consistent execution across dozens of simultaneous projects in markets with varying infrastructure readiness. As explored in our analysis of why India’s data center boom is an execution problem, not an announcement problem, the gap between announcement and delivery has been the defining feature of previous cycles and shows no sign of disappearing in this one.

The operators who will capture the most value from India’s data center growth cycle are those who treat execution as the primary constraint rather than capital or demand, because both capital and demand are available in abundance. Execution is the variable that will determine whether India’s data center market delivers on its announced ambitions or produces another cycle of impressive investment headlines and slower-than-projected capacity delivery.