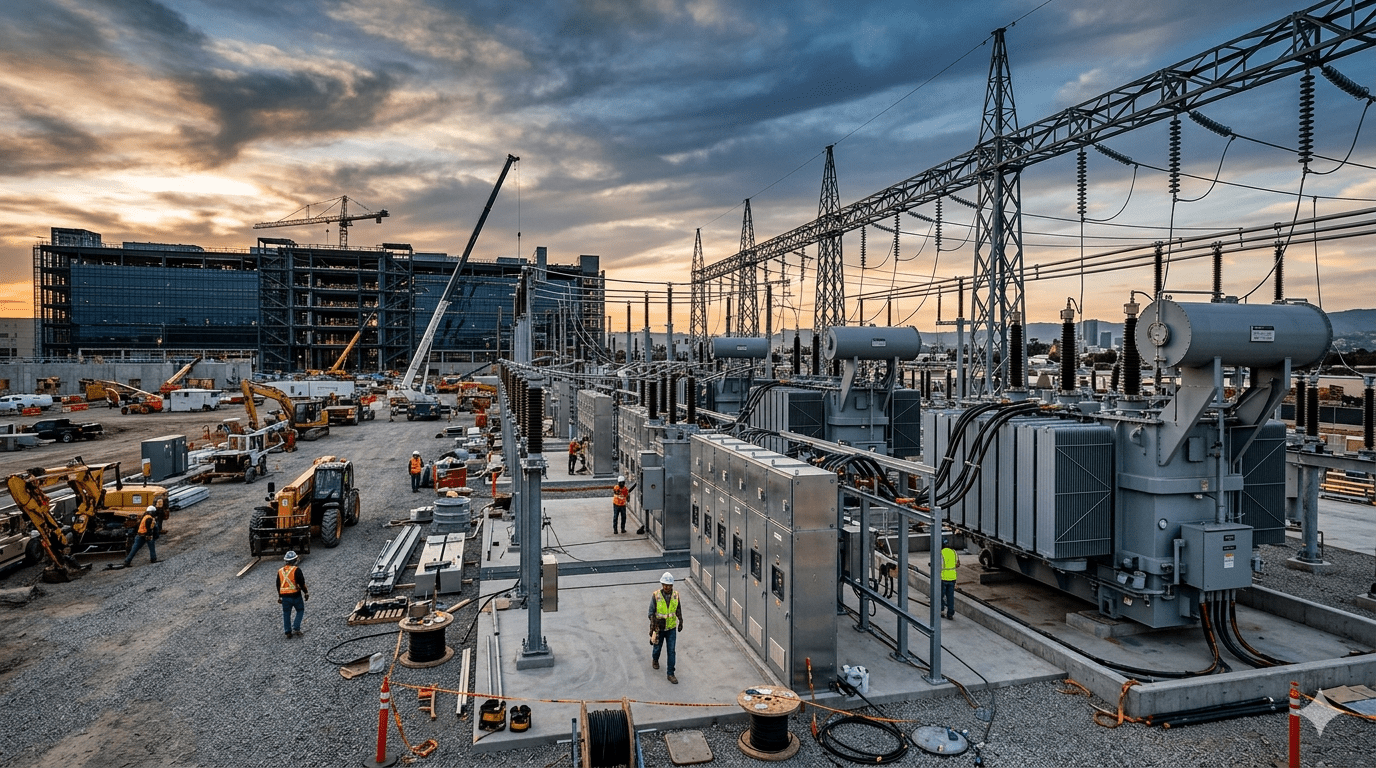

For most of the past century, the electrical equipment industry served a broad and diversified customer base. Utilities bought transformers and switchgear to upgrade aging grid infrastructure. Industrial manufacturers bought power distribution equipment to electrify new facilities. Commercial real estate developers bought medium-voltage switchgear for office towers and hospitals. No single customer category was large enough to reshape the production economics, lead times, or design priorities of the entire supply chain. That structural reality has changed. According to a new Wood Mackenzie report published this week, the US data center electrical equipment market is projected to grow from approximately $20 billion in 2026 to $65 billion by 2030. Data centers now account for roughly 68% of US load growth, a share large enough to make them the defining customer for an entire industrial sector.

The most striking figure in the Wood Mackenzie analysis is the transformer demand projection. Annual transformer demand from data centers could exceed 9,000 units by 2030, up from roughly 1,500 today. That sixfold increase in transformer demand from a single customer category is not a supply chain stress test. It is a supply chain transformation. Transformer manufacturing capacity that was sized for a diversified customer base must now accommodate a concentrated, rapidly growing demand source that is procuring at volumes, on timelines, and to technical specifications that existing manufacturing capacity was not designed to serve. Furthermore, data centers are moving earlier in the procurement cycle, locking in supply agreements years ahead of deployment rather than ordering equipment on conventional lead times. That shift in procurement behaviour is itself reshaping how transformer manufacturers plan their production capacity.

What This Means for the Supply Chain

The electrical equipment supply chain is not a market that responds quickly to demand signals. Building a new transformer manufacturing facility takes years of planning, capital investment, and workforce development. The lead times for large power transformers were already stretching beyond two years before the AI infrastructure buildout began accelerating in 2023. As data center demand has surged, those lead times have extended further, with some custom transformer orders now requiring commitments three to four years in advance of the installation date. For a data center developer whose entire business model depends on bringing capacity online quickly, a three-to-four-year transformer lead time is not a procurement challenge. It is a project timeline constraint that governs everything else.

The switchgear and power distribution equipment supply chain faces similar dynamics. Schneider Electric vice president of innovation Steve Carlini noted that operators are moving to prefabricated electrical systems to address labor shortages and rising density requirements, shifting demand toward factory-assembled solutions that deploy faster than site-built alternatives. Consequently, the manufacturers of prefabricated electrical infrastructure are experiencing demand growth that their existing production capacity cannot absorb without significant investment in manufacturing expansion. The Wood Mackenzie projection of $65 billion in annual electrical equipment demand by 2030 implies a manufacturing buildout requirement that is itself an infrastructure investment story of considerable scale.

The Procurement Behaviour That Is Reshaping Manufacturing

The shift in data center procurement behaviour toward multi-year advance commitments is creating a new market structure in the electrical equipment industry that benefits incumbent manufacturers with existing customer relationships and penalises new entrants who cannot offer the supply certainty that hyperscalers require. A transformer manufacturer that can credibly commit to delivering 500 units per year on a four-year rolling contract has a fundamentally different competitive position than one that can only offer spot market availability. The hyperscalers and large data center developers who are signing those multi-year supply agreements are simultaneously securing their own supply chains and concentrating market power among the manufacturers capable of honouring long-term volume commitments.

Additionally, the technical specifications of data center electrical equipment are diverging from the specifications that serve other customer categories in ways that are creating product-line specialisation within the electrical equipment industry. High-density data centers require transformers designed for the load profiles imposed by AI GPU clusters, including rapid load fluctuations that conventional transformer designs do not handle well. They require switchgear rated for the fault currents that large battery energy storage systems introduce into facility electrical architectures. As covered in our analysis of the transformer substation supply chain as an AI bottleneck, the technical demands of AI infrastructure are not simply a scaled-up version of conventional data center requirements. They are qualitatively different in ways that require product development investment from electrical equipment manufacturers.

The Geography of Supply Chain Stress

The geographic concentration of US data center development in Northern Virginia, Texas, Ohio, Phoenix, and a handful of other primary markets concentrates supply chain stress from electrical equipment demand rather than distributing it evenly across the country. Substation construction, transformer installation, and switchgear deployment for these markets are creating localized demand spikes that regional electrical contractors, utility coordination teams, and installation crews cannot absorb without importing capacity from other regions. In Northern Virginia, the world’s largest data center market by installed capacity, substation construction timelines have begun to dictate project delivery dates because the local contractor ecosystem cannot support the simultaneous buildout of multiple large facilities.

The Wood Mackenzie projection of $65 billion in annual electrical equipment demand by 2030 implies not just manufacturing expansion but also a parallel expansion in the installation and commissioning workforce that brings that equipment into service. Electrical equipment that is manufactured but cannot be installed on schedule because qualified crews are not available does not solve the supply chain problem. It relocates it from manufacturing to installation. The data center industry’s growing awareness of this dynamic is producing investment in electrician apprenticeship programs and electrical contractor capacity development that mirrors the investment in transformer manufacturing capacity. However, the workforce development timeline is even longer than the manufacturing capacity timeline, because training a qualified electrician takes years rather than months. The electrical equipment supply chain for AI infrastructure is being rebuilt from the ground up, and the rebuild will take longer than the demand curve that is driving it.