The Sentence That Erased Billions in an Afternoon

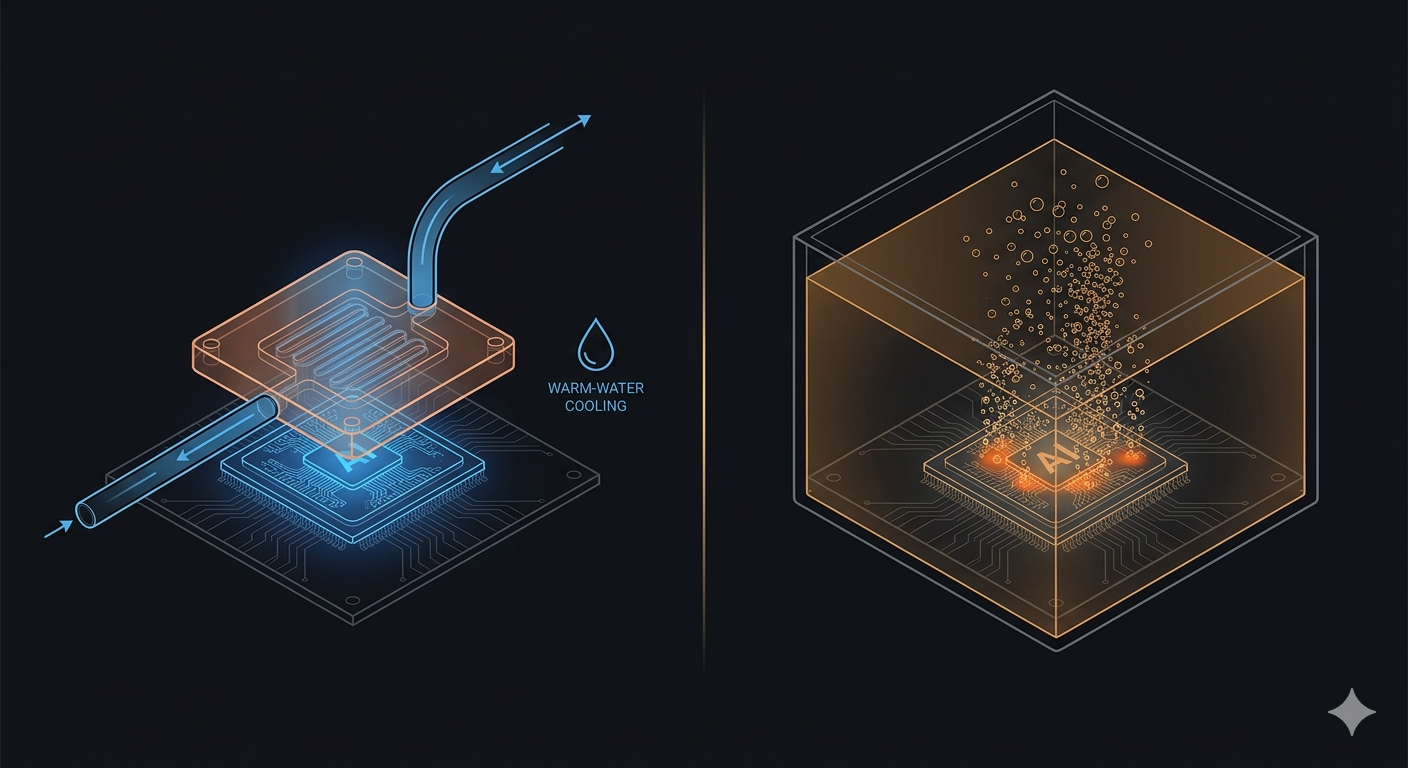

Jensen Huang did not announce a product failure. He announced an efficiency breakthrough, and the market punished an entire industry for it within hours. Standing on stage at the Consumer Electronics Show in Las Vegas in January 2026, Nvidia’s chief executive described how the company’s next-generation Vera Rubin platform would be cooled. The power of Vera Rubin is twice as high as Grace Blackwell, he told the audience, and yet the airflow into the system stays roughly the same. The water going into it, he continued, sits at exactly forty-five degrees Celsius. At that temperature, no water chillers are necessary for data centres. We are basically cooling this supercomputer with hot water, Huang said. It is so incredibly efficient.

Within minutes, the financial consequences of that sentence began registering on trading screens. Johnson Controls fell six point two percent. Modine Manufacturing dropped more than seven percent. Trane Technologies slid four percent. Carrier Global dipped nearly one percent. These are not marginal players in industrial cooling. They are the companies that have spent the past two years marketing themselves to investors as direct beneficiaries of the AI data centre boom, companies whose quarterly earnings calls increasingly opened with data centre order book updates. Baird’s equity analysts captured the market’s discomfort precisely in a note published that same day: we don’t see a big risk to near-term estimates, they wrote, but expect news to create some incremental concerns around orders, especially later in 2026.

The selloff was not really about one chip generation. It was a referendum on a deeper structural question the entire cooling industry had been avoiding: what happens to the chiller business when the chips themselves no longer need chilled water to run safely. Vera Rubin’s hot water architecture did not merely improve on the previous generation’s efficiency. It removed an entire category of equipment from the data centre cooling stack, and the market reacted to that removal exactly the way markets react to disintermediation anywhere else, by repricing every company sitting in the path of the disrupted layer.

What followed that January announcement was not a single story but several interlocking ones, unfolding across the months since: a genuine technical reordering of what liquid cooling means at the chip level, a scramble among hardware vendors to capture the coolant chemistry and infrastructure opportunity the shift created, and a parallel, almost unnoticed transformation in how the industry thinks about the heat itself, treating what was once pure waste as a commodity with a price. Understanding all three threads together explains why this single CES keynote moment became the defining inflection point of data centre cooling in 2026.

\What Vera Rubin Actually Changes

A Rack That Has No Air-Cooled Option at All

Vera Rubin is not a chip. It is a complete rack-scale redesign, and understanding why its cooling requirement is non-negotiable requires understanding the power density it operates at. The flagship configuration, the Vera Rubin NVL72, packages seventy-two Rubin GPUs and thirty-six custom Vera CPUs inside a single rack enclosure, delivering 3.6 exaflops of compute through NVLink 6 interconnects running at 260 terabytes per second of all-to-all bandwidth. Each individual Rubin GPU carries a thermal design power between one thousand eight hundred and two thousand three hundred watts, nearly double the one thousand two hundred watts that Blackwell’s GPUs drew. Multiply that across seventy-two GPUs in a single rack, and the resulting power draw lands somewhere between one hundred ninety and two hundred thirty kilowatts, depending on workload, compared to one hundred forty kilowatts for the previous-generation Blackwell GB300 NVL72.

At that density, air simply cannot move enough thermal energy away from the silicon fast enough to keep the chips within safe operating temperature. Nvidia did not build an air-cooled configuration as a fallback option. There is no air-cooled Rubin SKU at any thermal design power point. This is, in the most literal engineering sense, the moment liquid cooling stopped being a premium upgrade for the highest-density facilities and became the baseline entry requirement for running the most advanced AI hardware in the world. A data centre operator cannot choose to defer the liquid cooling investment and run Vera Rubin on legacy air-cooled infrastructure. The hardware will not function that way.

What makes the forty-five degree Celsius detail genuinely remarkable is not the temperature threshold alone, but what it implies about the thermal engineering inside the chip package itself. Conventional direct liquid cooling systems still typically run a chilled water loop, water actively cooled by a mechanical chiller down to somewhere in the range of eighteen to twenty-two degrees Celsius, because the cold plates attached to the chips needed that margin to extract heat fast enough. Vera Rubin’s architecture extracts heat efficiently enough at the chip interface that the incoming coolant can arrive nearly at room temperature by industrial standards, and still keep the silicon within its operating envelope. That is the specific engineering achievement Huang was describing as miraculous, and it is the reason the mechanical chiller, the single most capital-intensive and energy-hungry piece of equipment in a conventional data centre cooling plant, suddenly becomes optional.

Why Removing the Chiller Is Not the Same as Removing Cooling

The most important technical nuance lost in the immediate market panic was the distinction between eliminating chillers and eliminating cooling infrastructure altogether, and the industry’s most experienced liquid cooling vendors moved quickly to correct that conflation publicly. Vertiv issued a direct statement clarifying the point: using higher-temperature water does not eliminate the need for heat rejection, the company said. While approaches to heat rejection may change in a forty-five-degree Celsius water-cooled design, cooling infrastructure is still required, with architectures shifting toward liquid-to-liquid heat transfer or dry-cooler-based approaches rather than removing cooling systems entirely.

That distinction matters enormously for how the industry should actually be reading the stock market’s reaction. A dry cooler is fundamentally simpler equipment than a chiller. It rejects heat to the outside air using fans and heat exchange coils, without the compressor, refrigerant loop, and mechanical refrigeration cycle that a chiller requires. Dry coolers are cheaper to install, cheaper to maintain, and dramatically more energy-efficient to operate, because they are not consuming electricity to actively pump heat against a thermal gradient. They simply move warmer water past ambient air and let the temperature differential do the work. Replacing chillers with dry coolers is not the elimination of an entire cooling supply chain. It is a substitution of one type of heat rejection equipment for another, and crucially, it is a substitution that favours an entirely different set of suppliers than the ones who have dominated the conventional chiller market for decades.

This is precisely the distinction Joe Capes, chief executive of liquid cooling specialist LiquidStack, made in comments to Facilities Dive shortly after Huang’s announcement. Vera Rubin is a clear signal that the industry has crossed a threshold where liquid cooling is purposely integrated with the newest market-leading chips supporting AI deployments, Capes said. More efficient chips enable more compute per rack, which concentrates heat and raises the importance of liquid cooling. Capes added a further technical wrinkle worth noting: chillers could still play a role in data halls running exclusively on Vera Rubin architecture, specifically because of the high temperatures involved in the secondary water loop that ultimately rejects heat to the outside environment, and that high loop temperature may actually expand opportunities to use dry coolers for free cooling, rejecting heat into cooler outdoor environments rather than relying on energy-intensive mechanical refrigeration. The net effect, in his reading, is more free cooling and potentially less of the evaporative cooling that has drawn sustained criticism over data centre water consumption.

The Industry Splits in Two

Who Wins When the Chiller Disappears

The competitive consequence of Vera Rubin’s cooling architecture is not subtle, and it explains precisely why the market reaction divided so cleanly along lines that mirrored each company’s existing liquid cooling exposure rather than its overall data centre revenue. Industry analysts following the announcement specifically flagged nVent and Vertiv as companies positioned to benefit from Vera Rubin’s proliferation, precisely because both already held strong, established positions in liquid cooling infrastructure, coolant distribution units, manifolds, and the rack-level plumbing that direct-to-chip and immersion systems require. These companies were not threatened by the disappearance of the chiller. They had already built their growth strategy around the assumption that chip-level liquid cooling, not facility-level air conditioning, was the future of the category.

The companies whose stocks fell hardest tell a parallel and equally clear story. Johnson Controls, which had been actively reorienting its business strategy away from residential and light commercial HVAC customers in favour of North American data centre operators specifically because that segment had been a reliable growth engine, was particularly exposed to the Vera Rubin announcement, and its share price reflected that exposure with the sharpest single-day decline of the group. Modine Manufacturing, Trane Technologies, and Carrier Global all carry meaningful chiller product lines that have historically depended on data centre customers needing mechanical refrigeration capacity at facility scale. None of these four companies had built a comparable liquid cooling position to match Vertiv’s or nVent’s, and the market’s instant differentiation between the two groups was, in effect, a real-time referendum on which companies had correctly anticipated where the industry’s technology curve was heading.

The phrase one analyst quoted by Fierce Network used to frame the shift captures the mechanics precisely: if being able to support Vera Rubin chips with forty-five degree Celsius water means you don’t need a chiller, the analyst observed, then instead of buying a chiller you’re going to buy a dry cooler, which probably isn’t going to come from your traditional heat rejection supplier. That single sentence describes a genuine supply chain reshuffling event. The customer relationship, the procurement budget, and the engineering specification all shift toward a different category of vendor, and incumbents without an existing position in that category face a structural threat that has nothing to do with their execution quality and everything to do with which side of the chiller-to-dry-cooler transition they happen to sit on.

The Retrofit Bill Coming Due for Existing Facilities

Beyond the public market repricing of cooling equipment vendors, Vera Rubin’s hard liquid cooling requirement creates an immediate and unavoidable capital expenditure decision for every commercial real estate investor and data centre operator currently holding facilities built around earlier-generation infrastructure. Analysis aimed specifically at commercial real estate investors evaluating data centre acquisitions has been blunt about the scale involved. Retrofit costs for cooling infrastructure alone range from five hundred to one thousand five hundred dollars per kilowatt, translating to between sixty thousand and one hundred ninety-five thousand dollars per NVL72 rack. Scale that to a one hundred rack deployment, a modest size for a serious AI training facility, and the retrofit bill lands between six million and nineteen point five million dollars, before accounting for the separate cost of installing the new eight hundred volt direct current power architecture that Vera Rubin also requires.

This is not an optional upgrade that operators can defer while continuing to serve existing customers profitably on legacy infrastructure. The same analysis frames the choice facing operators of older facilities in stark binary terms: retrofit at significant cost, or risk obsolescence as tenants migrate toward AI-ready facilities that can actually host the hardware their workloads demand. For investors who acquired data centre real estate on the assumption that the asset’s value derived primarily from its land, power connection, and shell structure, Vera Rubin’s arrival recalibrates that valuation logic toward a much narrower question: does this specific building already have, or can it cost-effectively acquire, the direct liquid cooling infrastructure that next-generation AI hardware requires as a baseline, non-negotiable specification.

There is a partially offsetting factor that the same analysis is careful to note, because it meaningfully changes the economics for facilities that have already made some investment in liquid cooling capability. Rack airflow requirements fall by roughly eighty percent under the Vera Rubin architecture, which partially offsets the cooling investment for facilities that already possess some liquid cooling capacity, because the air handling infrastructure those facilities still need to maintain shrinks substantially in scale and cost. A facility caught in the middle, one that invested in hybrid air-and-liquid infrastructure during the Blackwell generation but has not yet committed fully to chip-level direct liquid cooling at scale, is positioned more favourably than a facility that remained purely air-cooled, but still faces a meaningful capital outlay to reach full Vera Rubin compatibility.

The Race to Build Around Rubin

Supermicro’s Bet on Speed and a New Kind of Coolant

While the equity markets were repricing established HVAC vendors, server manufacturer Supermicro moved aggressively to position itself as the fastest path to market for operators wanting to deploy Vera Rubin at scale. In January 2026, the company announced expanded manufacturing capacity and liquid cooling capabilities developed in direct collaboration with Nvidia, explicitly designed to enable first-to-market delivery of data centre-scale solutions optimised for both the Vera Rubin NVL72 and the smaller HGX Rubin NVL8 configuration. The company’s chief executive, Charles Liang, framed the positioning in terms of speed: Supermicro’s long-standing partnership with Nvidia and our agile building block solutions enable us to bring the most advanced AI platforms to market faster than others, he said.

The specifications Supermicro disclosed for its Rubin-ready systems illustrate just how comprehensively the cooling architecture has been redesigned around the new thermal requirements. The company’s implementation incorporates what it describes as an enhanced data centre-scale liquid cooling technology stack built around in-row coolant distribution units, enabling what Supermicro calls scalable warm-water cooling operation specifically engineered to minimise both energy consumption and water usage while simultaneously maximising rack density and overall thermal efficiency. This is a meaningfully different design philosophy from earlier liquid cooling generations, which often treated water conservation as a secondary consideration behind raw thermal performance. Warm-water operation at scale changes that calculus, because a system that does not require active chilling in the first place has fundamentally less embedded water and energy cost to optimise away.

Then, in June 2026 at Computex in Taipei, Supermicro escalated the materials science dimension of the competition directly, unveiling a proprietary dielectric coolant it calls SMC PG25-A, claiming the fluid achieves electrical impedance one thousand times higher than standard coolants currently used across the industry. The significance of that claim, if independently verified, is not abstract. Electrical impedance in a coolant directly determines what happens during a leak event inside a fully populated rack. A coolant with dramatically higher electrical impedance is far less likely to cause a short circuit or electrical fault if it makes contact with live components during a minor leak, which means a rack experiencing such a leak could potentially continue operating safely rather than triggering an immediate emergency shutdown. The framing one industry analysis used to describe the stakes is precise: the core technical question is whether a coolant’s electrical properties can make the difference between a rack worth roughly eight million dollars continuing to operate through a minor leak versus shutting down immediately. Supermicro paired the coolant announcement with a fully configured Vera Rubin NVL72 rack on display and a new end-to-end data centre blueprint explicitly designed to scale from five megawatts up to a full gigawatt of deployed capacity, with full deployments timed to align with Vera Rubin’s second-half 2026 general availability.

Ferveret and the Bet That Boiling Beats Pumping

While Supermicro and the established hardware vendors race to support Vera Rubin’s specific architecture, a smaller and more radical bet on the future of liquid cooling has been developing quietly out of MIT, built on physics borrowed directly from a completely different industry. Ferveret, founded by MIT associate professor Matteo Bucci and former MIT postdoctoral researcher Reza Azizian, takes its core thermal engineering insight from nuclear power plant cooling design, and the technology genuinely represents a different category of liquid cooling rather than an incremental refinement of existing direct-to-chip or immersion approaches.

The company’s system submerges computer servers in a specialised liquid engineered to absorb heat far more efficiently than air moved by a fan, which sounds, on its surface, similar to conventional immersion cooling already deployed across parts of the industry. What distinguishes Ferveret’s specific approach is a phenomenon happening at the microscopic surface of the server components themselves: smaller bubbles form at the server surface that detach more frequently than in conventional immersion fluids, and that more frequent bubble detachment accelerates the heat transfer process considerably beyond what static liquid contact alone achieves. This is, in essence, controlled boiling, the same physical principle nuclear engineers have spent decades studying and optimising for reactor core cooling, where extracting heat reliably and rapidly from an intensely hot surface is a matter of genuine safety-critical importance rather than a performance optimisation.

The efficiency claims associated with the technology, while still requiring independent, large-scale verification beyond Ferveret’s own disclosures, are substantial enough to merit serious attention from an industry actively searching for the next generation of thermal management beyond what direct-to-chip cold plates can achieve. The company has reported cooling cost reductions in the range of ninety-six percent compared to conventional air-cooling approaches, alongside capital expenditure reductions of roughly sixty-eight percent for the cooling infrastructure portion of a new build or upgrade project. MIT’s own reporting on the venture situates it within the broader urgency driving this entire wave of innovation: data centres are projected to account for anywhere from nine to seventeen percent of total United States electricity usage by the end of the decade, and today, around a third of data centre electricity is already devoted purely to cooling the chips that run AI models. Reducing that cooling energy burden through more efficient phase-change physics, rather than simply moving more water faster through bigger pipes, represents a genuinely distinct technical pathway from the warm-water, single-phase cooling that Vera Rubin’s reference design uses, and the two approaches are likely to coexist and compete for different segments of the market rather than one simply displacing the other.

The Heat Itself Becomes a Product

Why Forty-Five Degrees Changes the District Heating Calculation

The most consequential second-order effect of Vera Rubin’s hot water architecture has almost nothing to do with how the chips are cooled and everything to do with where the heat goes afterward, and it connects directly to a regulatory transformation already well underway across Europe before Vera Rubin existed. Direct liquid cooling systems extracting heat at the GPU die typically produce a coolant exit temperature in the range of fifty-five to sixty-five degrees Celsius, a range that falls squarely within the direct-injection compatibility window of fourth-generation district heating networks, the modern, lower-temperature municipal heating infrastructure increasingly common across northern Europe, without requiring any additional heat-boosting equipment to raise the temperature further before injection into the network.

That compatibility matters enormously because it eliminates the single most expensive piece of equipment in older waste heat recovery designs: the industrial heat pump needed to lift lower-temperature waste heat up to a level municipal networks could actually use. Article 26, paragraph 6 of the European Union’s recast Energy Efficiency Directive makes the assessment of waste heat reuse a legal obligation, not a voluntary sustainability initiative, for any data centre facility exceeding one megawatt of total rated energy input. Operators must conduct and submit a formal waste heat recovery feasibility assessment to national authorities before commissioning a qualifying facility, must implement waste heat reuse measures unless they can demonstrate a certified infeasibility through documented technical or economic barriers, and must report annually on the actual percentage of total thermal output successfully recovered and reused. Regulators in Germany, the Netherlands, and Denmark have consistently rejected infeasibility claims on cost grounds wherever a fourth-generation district heating pipe already exists within two kilometres of a facility’s boundary, signalling that the exemption pathway is considerably narrower than many operators initially assumed it would be.

Germany has gone further than the broader EU framework, embedding specific numerical targets directly into national law through its Energy Efficiency Act. Starting from July 2026, new data centres in Germany must demonstrate and utilise at least ten percent of their generated waste heat, with that mandated share rising to fifteen percent in 2027 and at least twenty percent by 2028, contingent on technical and economic feasibility assessments. France has set its own binding obligations targeting fifteen to twenty-five percent reuse by 2030 through 2035. Sweden and Denmark are targeting twenty-five to thirty-five percent by the 2025 to 2030 window, while the Netherlands aims for twenty to thirty percent by 2030. None of these national targets were written with Vera Rubin’s specific thermal output in mind, but the platform’s native fifty-five to sixty-five degree coolant exit temperature happens to align almost perfectly with what these regulatory frameworks were designed to capture, turning a compliance obligation into something closer to a straightforward commercial opportunity for operators who build their facilities correctly from the outset.

What Heat Is Actually Worth Today, in Real Projects

The commercial reality of selling waste heat has moved well beyond pilot programmes and into operating infrastructure generating measurable revenue, and the scale of some of these projects is genuinely substantial. In Finland, a major hyperscaler partnered with the energy company Fortum to construct what both parties describe as the world’s largest data centre waste heat recycling project, with combined thermal power capacity reaching up to three hundred fifty megawatts. Once fully operational across the 2025 to 2026 heating season, the project is expected to supply approximately forty percent of district heating demand for an entire metropolitan area serving two hundred fifty thousand residential and commercial customers. Fortum invested roughly two hundred twenty-five million euros into the heat pump plants and pipeline infrastructure the project required, an investment the company expects to eliminate approximately four hundred thousand tonnes of carbon dioxide emissions annually once the system reaches full operational capacity.

Google’s Hamina facility in Finland represents a different but equally instructive model, because it was the company’s first offsite heat recovery project anywhere in the world and has operated long enough to generate genuine performance data. A seven and a half megawatt heat pump plant connected through a one point three kilometre pipeline supplies forty gigawatt-hours of district heating annually, covering eighty percent of the local city’s total heating demand, with Google supplying that heat free of charge to the municipal utility rather than charging for it directly. Microsoft has pursued a comparable model in Denmark, with its Høje-Taastrup facility feeding waste heat into the local district network, while the Tallaght District Heating Scheme in Ireland, drawing waste heat from a nearby Amazon facility, saved one thousand one hundred tonnes of carbon dioxide emissions in its very first year of operation. In the United Kingdom, London’s mayor has announced plans for a new district heat network specifically designed to supply over nine thousand homes using waste heat recovered from local data centres, even though the UK currently has no binding national mandate requiring such reuse.

The economics underlying these projects are becoming genuinely standardised enough to model with reasonable confidence. Industry analysis places thermal energy offtake pricing in the range of fifteen to thirty dollars per megawatt-hour for facilities connecting through more conventional arrangements, while facilities able to inject heat directly at fifty-five to sixty-five degrees Celsius into fourth-generation networks, precisely the temperature range Vera Rubin’s direct liquid cooling system produces, can command twenty-five to forty-five euros per megawatt-hour because they avoid the capital and operating cost of an intermediate heat pump entirely. For a one hundred megawatt AI campus situated near an existing municipal heating network, that pricing structure translates into an estimated twenty-five to thirty-five million euros in annual heat sales revenue, a figure substantial enough that waste heat recovery has shifted, in the words of one detailed 2026 industry guide, from sustainability pilot to standard design consideration for any new European AI campus above one megawatt. Markus Blüm, managing director of Green Mountain KMW Data Center, offered the practical caveat that governs where this economic logic actually applies: if you want to use the heat from the data centre, it only works if the facility is close to the existing district heat system, he told a Frankfurt industry panel in May 2026. There’s no business case to transport thirty degree Celsius heat over five to ten kilometres.

Why the Nordics Got There First and What That Reveals About the Roadmap Elsewhere

The geographic concentration of operational waste heat recovery projects in Finland, Sweden, and Denmark is not coincidental, and understanding why those specific markets moved first illuminates the structural conditions other regions will need to replicate before similar economics become available to them. Finland, Sweden, Denmark, and Norway already routinely integrate data centre waste heat into district heating networks as a matter of established practice rather than emerging innovation, a pattern that reflects decades of prior investment in district heating infrastructure itself, infrastructure that exists in these countries for reasons entirely unrelated to data centres, built originally to serve cold-climate residential and commercial heating demand at a national scale that few other regions, including most of the United States, ever developed.

This pre-existing infrastructure advantage matters enormously for project economics, because the single most consistent variable determining whether a waste heat recovery project pencils out financially is proximity to an existing district heating main, not the underlying technical sophistication of the heat capture system itself. Analysis of more than twenty operating projects found that when data centres are located within one to two kilometres of an existing district heating main, the simple payback period for the heat network investment commonly falls below eight to ten years, and can be considerably shorter where carbon pricing or fuel taxes on competing gas heating sources push the comparative economics further in the data centre operator’s favour. The economics deteriorate quickly once that distance grows beyond three to four kilometres, unless the local heat demand density is exceptional enough to justify the additional pipeline investment regardless.

The case study Adamski and colleagues documented, examining waste heat reuse at a university campus connected to a district heating network, illustrates the kind of granular performance data the field has now accumulated. Their study found heat reuse efficiency capped at eighty-nine and a half percent, with simulations of an expanded data centre infrastructure predicting a fifty-eight percent reduction in carbon emissions compared to nearby buildings relying on conventional heating, alongside annual cost savings of approximately four hundred fifty thousand euros against an initial capital investment of three million euros, producing an estimated return on investment of six point seven years. Markets without this pre-existing district heating backbone, most of the United States chief among them, face a structurally different calculation: building the heat network infrastructure essentially from scratch alongside the data centre itself, rather than connecting into capacity that already exists, which is precisely why waste heat reuse remains overwhelmingly a European phenomenon at meaningful operational scale even as American data centre construction vastly outpaces European construction in raw volume.

What the Splintered Industry Looks Like From Here

Three Distinct Cooling Philosophies Now Competing Simultaneously

Stepping back from the individual companies and technologies, the genuine significance of the past six months is that data centre cooling has stopped being a single, converging technology roadmap and has instead splintered into at least three philosophically distinct approaches, each backed by serious capital and serious engineering talent, each making a different bet about where the industry’s constraints will actually bind hardest over the coming several years. Nvidia’s Vera Rubin reference design, built around warm-water single-phase direct liquid cooling at forty-five degrees Celsius, bets that the binding constraint is energy efficiency and chiller elimination, optimising for a power-constrained world, in Huang’s own framing, where every watt not spent on mechanical refrigeration is a watt available for additional compute.

Supermicro’s parallel bet, building manufacturing capacity and coolant chemistry specifically engineered around leak safety and rapid deployment speed, treats reliability and time-to-market as the binding constraint, recognising that hyperscalers racing to deploy Vera Rubin capacity at gigawatt scale need infrastructure partners who can move at the same velocity as Nvidia’s own product cycle, and who can give operators confidence that a coolant leak inside an eight-million-dollar rack will not necessarily mean catastrophic, immediate failure. Ferveret’s boiling liquid approach, drawing directly on nuclear engineering physics, bets that neither of the other two philosophies goes far enough, and that genuine step-change reductions in both energy consumption and capital cost require abandoning incremental refinement of pumped liquid loops altogether in favour of phase-change physics that extracts heat through a fundamentally more efficient mechanism.

Layered above all three of these competing technical philosophies sits the waste heat economy, which does not compete with any of them directly but instead determines which approach generates the most additional commercial value once the primary cooling job is done. A facility running Vera Rubin’s reference design, producing coolant at temperatures naturally compatible with European district heating networks, is positioned to capture meaningful incremental revenue that a facility running a different cooling architecture at a different exit temperature simply cannot access as easily. This is not a minor footnote to the cooling story. It is becoming, in markets with mature district heating infrastructure, a genuine factor in which cooling architecture an operator chooses, alongside the more familiar considerations of capital cost, energy efficiency, and chip compatibility.

What ties all of this together, and what makes the period since January’s CES keynote genuinely historic rather than merely another product cycle, is that the chiller, the single piece of equipment that has anchored data centre mechanical design for the entire history of the industry, is no longer a default assumption. It has become a choice, one increasingly made not by facilities engineers selecting from a stable, mature product category, but by silicon architects designing chips with a specific water temperature already built into the package specification. The cooling industry did not choose to split in two. Nvidia’s chip roadmap split it, and every vendor in the space, from the largest publicly traded HVAC conglomerate to the smallest MIT spinout, is now repositioning around a thermal architecture decision that was made, fundamentally, inside a semiconductor design team rather than a mechanical engineering department.