Data center site selection used to start with a relatively short checklist. Grid capacity. Land availability. Fiber connectivity. Labour market. Permitting environment. Those factors still matter. What has changed is the order of priority and the weight assigned to each one. Behind-the-meter power generation has moved from a niche consideration to a mainstream strategic option. It is, in turn, reshaping how developers evaluate sites, structure deals, and think about total cost of ownership over a twenty-year asset life.

The shift has a straightforward cause. Grid interconnection timelines in primary AI infrastructure markets have extended to five, seven, and in some cases ten or more years. A developer who secures planning permission and completes construction in twenty-four months can still be waiting three years for a grid connection. The facility sits ready but dark. Behind-the-meter generation solves that problem. It does not, however, solve it for free. The economics are, consequently, more complex than the headline narrative suggests.

How the Site Selection Calculus Has Changed

The traditional site selection model treated power as a utility input: available or not available, priced within a known range, and procured through a standard utility relationship. That model assumed grid connection timelines of twelve to eighteen months and power prices that were relatively stable over the planning horizon. Both assumptions have, notably, broken down in primary AI infrastructure markets. Grid connection timelines are now a primary constraint in Northern Virginia, Silicon Valley, Dallas, Chicago, and most major European data center markets. Power prices have moved materially higher in markets where AI load growth has driven utility investment. That investment gets, in turn, passed through to commercial customers.

Behind-the-meter generation changes the site selection calculus in two specific ways. First, it decouples the timeline to first power from the grid interconnection queue. A site that would require a five-year wait for a grid connection can, with behind-the-meter generation, be operational in twelve to eighteen months. That timeline advantage is, specifically, worth a significant premium. AI infrastructure customers are paying for capacity on deployment schedules that do not accommodate five-year waits. Second, it opens up sites that would not qualify under traditional grid-dependent models. Industrial land with existing gas infrastructure but no available grid capacity becomes, consequently, viable when behind-the-meter generation is part of the model. The Blog How Behind-the-Meter Power Is Reshaping AI Infrastructure covered the early phase of this shift. The market has, in turn, moved considerably further in the same direction since that analysis was published.

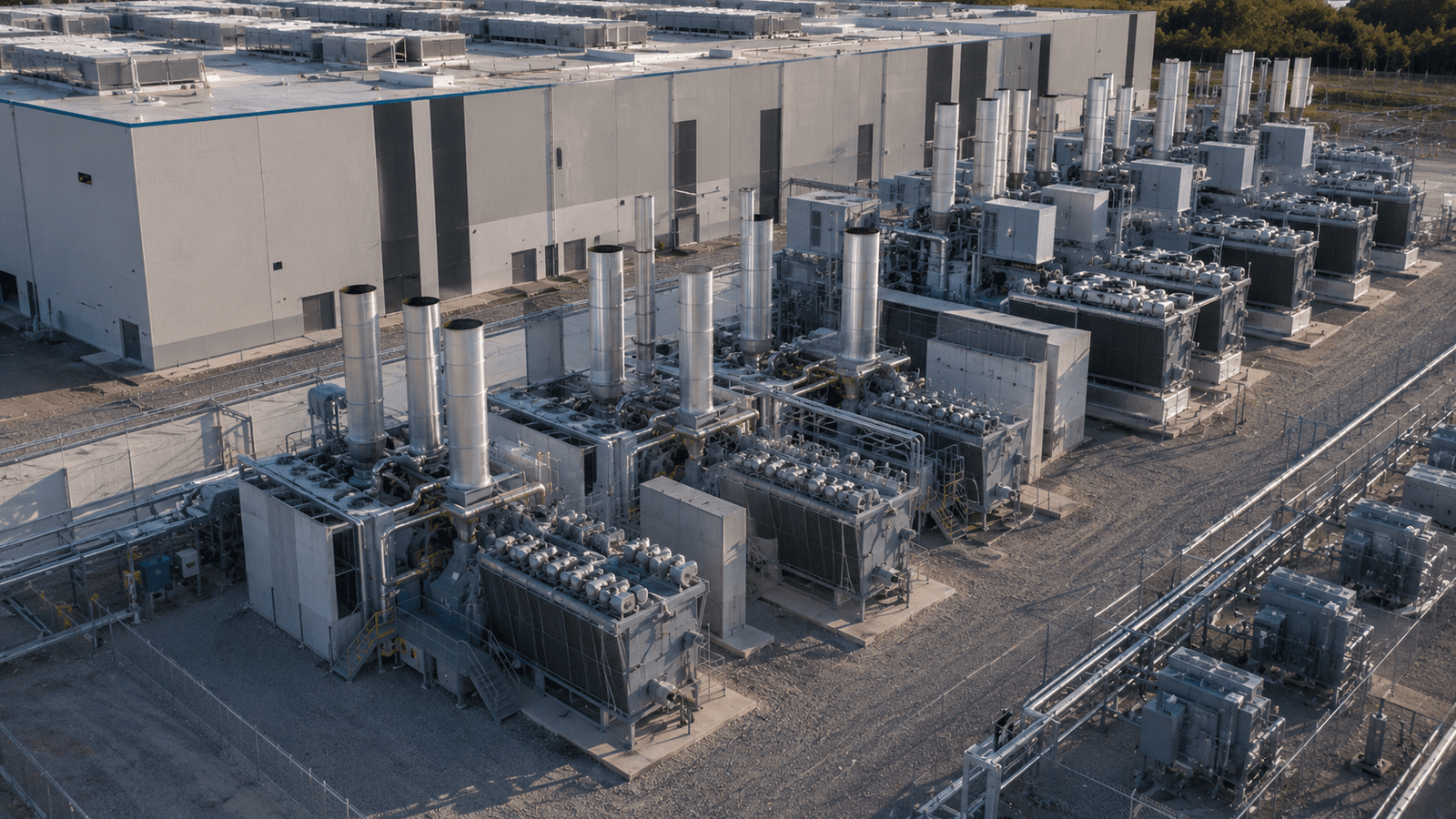

The Economics of Behind-the-Meter Generation

The economics of behind-the-meter generation are, however, more nuanced than the site selection conversation typically acknowledges. Natural gas reciprocating engines are the most common behind-the-meter technology for large data center deployments. Their fully-loaded cost runs between $0.06 and $0.10 per kilowatt-hour when capital, fuel, operations, and maintenance are included. That range overlaps with commercial grid pricing in many markets, which means behind-the-meter generation is not automatically cheaper. It is, rather, a trade that exchanges grid connection timeline risk for capital commitment and fuel price exposure.

The capital commitment is, specifically, substantial. A 100-megawatt behind-the-meter gas generation installation costs approximately $80 million to $120 million to build and commission. That capital deploys before the data center generates revenue. It sits on the balance sheet during construction and adds to the project’s financing cost. A data center running on behind-the-meter gas generation is, consequently, directly exposed to natural gas price movements. A grid-connected facility on a fixed-price utility tariff does not carry that exposure. The Long Read The Economics of Behind-the-Meter Power in AI Data Centers lays out the full cost structure in detail. The conclusion holds: behind-the-meter generation is a viable economic choice in specific circumstances, not a universal solution.

Those circumstances are, notably, becoming more common. The markets where behind-the-meter economics work best share four characteristics. Grid connection timelines are long. Gas infrastructure is available. The regulatory environment permits large-scale on-site generation. And the customer’s deployment timeline creates genuine value for faster access to power. In Northern Virginia, Texas, and parts of the Midwest, all four conditions are, in turn, frequently met simultaneously. In European markets, the regulatory environment is, however, more restrictive, and the economics are correspondingly less favourable for gas-based solutions.

What Developers Are Actually Doing

The most sophisticated data center developers are, specifically, not choosing between grid connection and behind-the-meter generation as an either-or decision. They structure projects that use behind-the-meter generation to reach first power quickly while maintaining a grid connection application in parallel. If that application is approved, the facility transitions to grid power and the on-site generation is redeployed or decommissioned. That hybrid approach captures the timeline advantage while hedging against the fuel price and capital commitment risks of a permanent off-grid model.

The VoltaGrid model, backed by Blackstone and Halliburton with $1 billion in fresh capital, is, notably, a direct bet on the durability of behind-the-meter demand from data center developers. VoltaGrid’s QPac modular generation platform is, specifically, designed for the hybrid deployment profile. It is scalable, fast to deploy, and available under a minor source air permit that avoids the regulatory delays of larger permanent installations. The Article AI Is Rewriting the Criteria for Data Center Site Selection examined how AI-specific requirements have changed site evaluation criteria broadly. Behind-the-meter generation is, in turn, the single factor that has changed most dramatically since that analysis.

The practical consequence for site selection is a new tier of evaluation criteria that did not exist three years ago. Developers are, consequently, now assessing gas pipeline proximity, air permit feasibility, and behind-the-meter generation capital cost as first-order variables. These sit alongside the traditional grid, land, and connectivity checklist. Sites that score well on both sets of criteria command, in turn, a material premium over those that meet only one.