Summary

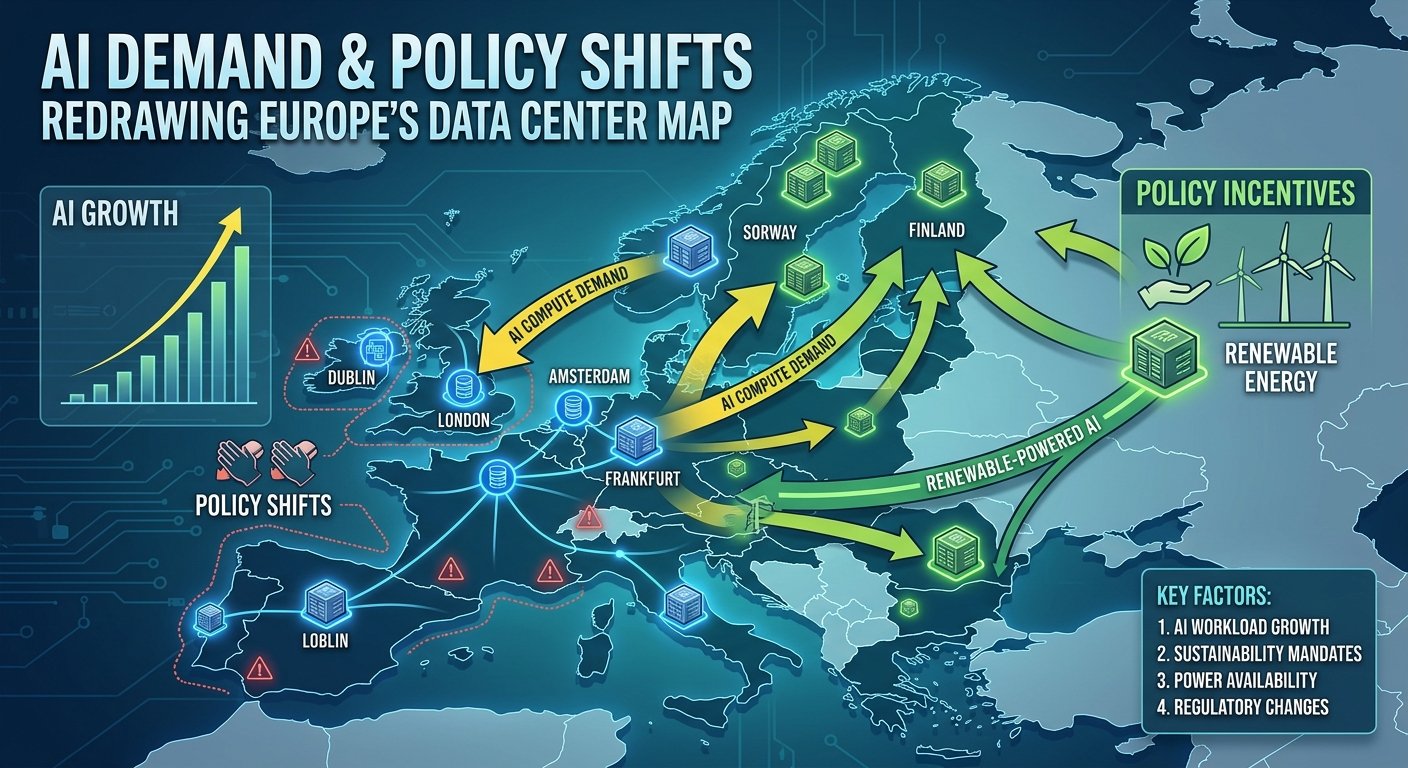

Europe’s data center industry is entering a period of structural change. For years, growth concentrated around a small group of established markets, particularly Frankfurt, London, Amsterdam, Paris, and Dublin. These cities became the foundation of Europe’s digital economy because they combined connectivity, financial activity, cloud adoption, and international business demand. The concentration of infrastructure created powerful network effects that reinforced their dominance. Hyperscale cloud providers, colocation operators, enterprises, and telecommunications companies all gravitated toward these locations. That model is now facing new pressures. Artificial intelligence, power constraints, sustainability requirements, and evolving government policies are changing the factors that determine where new data center capacity can be built. The result is a gradual redistribution of investment across the continent.

AI is accelerating this transformation because it introduces infrastructure requirements that differ significantly from those of traditional cloud workloads. Large language models, AI training clusters, and inference platforms require enormous amounts of electricity, advanced cooling systems, and high-density computing environments. These requirements place unprecedented pressure on energy networks and planning authorities. Markets that once enjoyed natural advantages now face constraints related to power availability, permitting timelines, and environmental regulations. At the same time, emerging locations are attracting attention because they offer access to renewable energy, available land, and less congested infrastructure networks. Europe’s next phase of data center growth is therefore becoming increasingly distributed rather than concentrated.

This shift is occurring alongside a broader policy evolution. European governments increasingly view digital infrastructure as a strategic asset tied to economic competitiveness, technological sovereignty, and AI leadership. New initiatives designed to expand cloud and AI capacity are encouraging investment while sustainability regulations are imposing stricter operating requirements. These parallel trends are reshaping the geography of infrastructure development. The future map of Europe’s data center industry will likely look very different from the one that defined the cloud era.

The End of the FLAP-D Monopoly?

Why Traditional Hubs Became Dominant

The rise of Frankfurt, London, Amsterdam, Paris, and Dublin was not accidental. These markets emerged as Europe’s leading data center destinations because they sat at the intersection of connectivity, economic activity, and digital demand. Financial institutions, multinational corporations, telecommunications providers, and internet exchanges all concentrated in these locations. The resulting ecosystem created strong incentives for infrastructure investment. Once cloud providers established major footprints, additional investment followed naturally.

Network density became one of the most important advantages. Data centers benefit from proximity to other infrastructure assets because connectivity remains a critical requirement for cloud services and enterprise applications. Organizations seeking low-latency access to customers often preferred locations already connected to major digital networks. This created a cycle in which growth reinforced existing advantages.

The cloud boom strengthened this dynamic further. As hyperscalers expanded across Europe, they concentrated much of their infrastructure within established hubs. Colocation providers followed closely because enterprises wanted access to the same ecosystems. By the early 2020s, the FLAP-D markets had become synonymous with European data center growth.

Yet the factors that created this dominance are no longer sufficient on their own. AI infrastructure places greater emphasis on energy availability, land access, and sustainability considerations. These requirements are exposing limitations within Europe’s most mature markets.

Capacity Constraints Are Changing the Equation

The challenge facing Europe’s traditional hubs is not demand. Demand remains exceptionally strong across nearly all major markets. The problem is the ability to convert that demand into deliverable capacity. Electricity access, permitting processes, environmental requirements, and land availability are increasingly determining where projects move forward. These constraints affect some of Europe’s largest markets more than others.

Power availability has emerged as one of the most important issues. In many established metropolitan areas, grid infrastructure was not designed to accommodate the scale of electricity demand associated with AI-driven data centers. Securing new connections can require years of planning and investment. Operators therefore face growing uncertainty regarding deployment timelines.

Permitting challenges add another layer of complexity. Environmental reviews, sustainability requirements, and local planning regulations can extend development schedules significantly. As demand accelerates, delays become more costly. Infrastructure investors are increasingly prioritizing locations where projects can progress with greater certainty.

AI Is Reshaping Infrastructure Priorities

Training and Inference Require Different Strategies

One of the most important shifts occurring within the AI ecosystem involves the changing balance between training and inference workloads. During the initial wave of generative AI investment, much of the industry’s attention focused on training large models. These environments require massive computing clusters and benefit from access to large-scale energy resources. Training workloads often prioritize electricity availability and operational efficiency over proximity to end users. Organizations can locate training environments in regions that offer abundant renewable energy, lower operating costs, and favorable environmental conditions. This flexibility creates opportunities for markets outside traditional metropolitan centers.

Inference introduces a different set of requirements. Once AI models are deployed, they must serve users with minimal latency. Inference workloads therefore benefit from proximity to businesses, consumers, and industrial environments. As AI adoption expands, demand for distributed inference infrastructure is expected to increase significantly. This distinction is important because it supports a more geographically diverse infrastructure landscape. Training and inference may increasingly occupy different locations depending on their specific operational requirements. Europe’s data center market is evolving to accommodate both models simultaneously.

AI Changes Site Selection Criteria

The rise of AI is altering how developers evaluate potential locations. Traditional cloud facilities often prioritized connectivity and customer proximity above all else. AI infrastructure still values these characteristics, but additional considerations now carry greater weight. Power availability, renewable energy access, cooling efficiency, and expansion potential have become critical decision factors. Energy infrastructure is particularly important because AI workloads consume far more electricity than many traditional enterprise applications. Facilities capable of supporting large GPU clusters require significant power resources. Developers increasingly evaluate regional energy ecosystems before making investment decisions.

Cooling requirements are also influencing site selection. High-performance AI environments generate substantial heat, making thermal management a critical operational concern. Regions with favorable climatic conditions may benefit from lower cooling costs and improved efficiency. These considerations are encouraging a broader distribution of infrastructure investment across Europe.

Emerging Markets Move Into the Spotlight

Southern Europe Is Attracting New Investment. Spain’s Position Is Strengthening

Spain has become one of the most closely watched data center markets in Europe. While Madrid has long maintained a presence within the continent’s digital infrastructure ecosystem, recent developments have elevated its strategic importance. The combination of renewable energy availability, expanding connectivity infrastructure, and increasing cloud investment is attracting attention from hyperscalers, colocation operators, and infrastructure funds. Unlike some of Europe’s most mature markets, Spain still offers opportunities for large-scale expansion in areas where power constraints are less severe. This flexibility is becoming increasingly valuable as AI workloads place greater pressure on electricity networks across the continent. Developers seeking long-term growth opportunities are therefore looking beyond traditional hubs toward markets capable of supporting future demand. Spain’s emergence reflects a broader trend in which infrastructure investment follows energy availability as much as connectivity advantages.

The country’s renewable energy profile is a particularly important factor. Spain has invested heavily in solar and wind generation over the past decade, creating an energy landscape that aligns well with the sustainability objectives of many technology companies. Access to renewable electricity has become a key consideration for organizations expanding AI infrastructure because energy consumption remains one of the largest operational costs associated with advanced computing environments. Developers increasingly view renewable energy access as both an economic and environmental advantage. As AI deployments continue expanding, regions capable of supplying clean electricity at scale may attract a growing share of infrastructure investment. Spain appears well positioned to benefit from this shift. The country’s role within Europe’s data center market is therefore likely to continue evolving.

Italy Is Becoming More Competitive

Italy is also attracting greater interest than it did during earlier phases of European data center development. Historically, the country received less attention than northern European markets because connectivity ecosystems and cloud infrastructure remained concentrated elsewhere. That situation is gradually changing as demand for digital services expands and infrastructure providers seek alternatives to saturated locations. Milan has emerged as a focal point for investment due to its economic importance and growing digital ecosystem. The city’s position within southern Europe makes it an attractive destination for organizations serving regional markets. Interest in AI infrastructure is further increasing the appeal of locations capable of supporting new development.

The Italian market illustrates how AI is broadening the range of viable infrastructure destinations. Traditional cloud deployments often gravitated toward established hubs because network effects created powerful advantages. AI introduces additional variables into site selection decisions, including power availability, land access, and cooling efficiency. These factors can favor locations that were previously considered secondary markets. Italy’s growing relevance reflects this broader reassessment of infrastructure priorities. As organizations evaluate future capacity requirements, the country’s position within Europe’s digital infrastructure landscape may continue strengthening. The trend demonstrates how the next phase of growth is becoming more geographically diverse.

The Nordic Advantage in the AI Era

Renewable Energy Is Becoming a Strategic Asset

The Nordic region has long attracted attention from data center operators because of its favorable environmental conditions and abundant renewable energy resources. Countries such as Sweden, Norway, Finland, and Denmark offer access to low-carbon electricity, cool climates, and stable political environments. These characteristics have supported data center development for many years. AI is increasing the strategic value of these advantages because advanced computing environments require enormous amounts of energy. Regions capable of supplying renewable power at scale are becoming increasingly attractive to infrastructure investors. The Nordic markets therefore occupy a unique position within Europe’s evolving data center landscape.

Energy availability plays a particularly important role in AI infrastructure planning. Training large models can require substantial electricity resources over extended periods. Operators seeking predictable energy costs and strong sustainability credentials often view the Nordic region favorably. Renewable generation helps support both objectives. At the same time, cooler climates can reduce cooling requirements, improving operational efficiency. These factors create a compelling combination for organizations evaluating long-term infrastructure investments. While the region may not replace traditional metropolitan hubs entirely, it is likely to play a growing role in supporting Europe’s AI ambitions. The Nordic advantage increasingly extends beyond sustainability into broader infrastructure competitiveness.

Eastern Europe Enters the Conversation

New Opportunities Beyond Established Markets

Eastern Europe is increasingly attracting attention from infrastructure investors seeking alternatives to saturated western European locations. Countries such as Poland are benefiting from growing digital economies, improving connectivity infrastructure, and increasing interest from cloud providers. These developments are creating new opportunities for data center expansion. While the region remains smaller than Europe’s traditional hubs, its strategic importance is rising as organizations seek greater geographic diversity. AI is accelerating this trend because emerging markets often possess development potential unavailable in more mature locations.

Poland has emerged as a particularly notable example. The country’s economic growth, central location, and expanding digital ecosystem have attracted investment from major technology companies. Connectivity improvements and cloud adoption are strengthening the market’s long-term prospects. At the same time, infrastructure developers view the region as an opportunity to expand capacity without encountering some of the constraints affecting western European hubs. These advantages are contributing to a broader reassessment of Eastern Europe’s role within the continental infrastructure landscape. The region’s importance is likely to increase as demand continues growing.

Infrastructure Investment Is Becoming More Distributed

One of the defining characteristics of Europe’s next infrastructure cycle is the increasing distribution of investment across multiple regions. The cloud era concentrated capacity within a relatively small number of metropolitan centers. AI is encouraging a more diversified approach because infrastructure requirements have expanded beyond connectivity alone. Power availability, sustainability considerations, and expansion potential are influencing site selection decisions in new ways. This shift creates opportunities for markets that previously occupied secondary positions within the European ecosystem.

The trend does not imply the decline of established hubs. Frankfurt, London, Amsterdam, Paris, and Dublin will remain central to Europe’s digital economy for the foreseeable future. However, future growth may be distributed more broadly across emerging locations. The combination of AI demand and policy changes is encouraging operators to evaluate a wider range of markets. This diversification may improve resilience while supporting regional economic development. The resulting infrastructure landscape is likely to be more balanced than the one that emerged during the early cloud era.

Sustainability Policy Is Reshaping Development

Environmental Regulations Are Influencing Investment

European policymakers increasingly view sustainability as a central component of infrastructure planning. Data centers have become part of broader discussions about energy consumption, carbon reduction, and resource management. New projects often face detailed scrutiny regarding environmental performance and long-term sustainability strategies. These considerations influence permitting decisions, operational requirements, and infrastructure investment priorities. Operators must therefore balance growth objectives with increasingly ambitious environmental expectations.

AI complicates this equation because advanced computing environments require significant energy resources. Policymakers face the challenge of supporting technological innovation while maintaining climate objectives. The resulting policy landscape is becoming more complex as governments attempt to balance competing priorities. Developers must navigate evolving regulations while ensuring that projects remain economically viable. Sustainability is therefore becoming a strategic factor rather than simply a compliance issue. Future infrastructure investment will likely reflect this reality.

Energy Efficiency Is Becoming a Competitive Differentiator

The emphasis on sustainability is encouraging greater attention to efficiency across the industry. Operators are investing in advanced cooling systems, renewable energy procurement, and energy management technologies designed to reduce environmental impact. These initiatives can also improve operational performance, creating benefits that extend beyond regulatory compliance. Efficiency is increasingly viewed as a competitive advantage within the AI infrastructure market.

The trend reflects a broader evolution in how organizations evaluate infrastructure performance. Energy consumption, carbon intensity, and resource utilization are becoming important decision factors alongside connectivity and reliability. As AI expands, these considerations are likely to become even more significant. Infrastructure providers capable of demonstrating strong sustainability performance may enjoy advantages in attracting customers and securing regulatory approval. The intersection between environmental policy and digital infrastructure is therefore becoming increasingly important.

Digital Sovereignty Is Becoming an Infrastructure Driver

Governments Increasingly View Data Centers as Strategic Assets

European governments are no longer approaching data centers solely as commercial real estate projects or supporting infrastructure for the digital economy. Policymakers increasingly view digital infrastructure as a strategic asset linked to economic resilience, technological competitiveness, and national security. The rapid growth of AI has accelerated this perspective because advanced computing capabilities are becoming central to innovation, research, and industrial development. Access to computing resources now influences a country’s ability to participate in emerging technology markets. As a result, governments across Europe are paying closer attention to where digital infrastructure is built and who controls it.

This policy shift is reshaping investment priorities throughout the region. Public-sector initiatives designed to support cloud infrastructure, high-performance computing, and AI development are creating new opportunities for data center operators. Infrastructure projects that align with broader national objectives may receive stronger institutional support than in previous years. Policymakers increasingly recognize that AI leadership depends not only on software innovation but also on the physical infrastructure capable of supporting advanced workloads. This understanding is influencing both regulatory frameworks and long-term development strategies. The data center industry is becoming more closely integrated into broader economic planning.

The emphasis on digital sovereignty is particularly important in Europe because the region continues to balance domestic technology ambitions with a global cloud ecosystem largely dominated by international providers. Governments want to ensure that organizations have access to secure and reliable computing resources while maintaining control over critical digital infrastructure. This objective is contributing to greater investment in regional capacity and encouraging discussions about long-term infrastructure independence. The outcome is likely to shape where future AI facilities are developed and how infrastructure ecosystems evolve over the next decade.

AI Policy Is Influencing Infrastructure Decisions

AI policy is emerging as another important factor in the evolution of Europe’s data center landscape. Governments are developing frameworks designed to encourage innovation while addressing concerns related to transparency, safety, and governance. These policies influence infrastructure development because AI systems require substantial computing resources. The ability to support advanced AI applications depends on the availability of appropriate infrastructure at scale.

Public and private investments in AI capacity are increasingly interconnected. National AI strategies often include objectives related to computing resources, cloud infrastructure, and digital innovation ecosystems. As governments seek to strengthen AI capabilities, infrastructure investment becomes part of a broader policy agenda. This relationship is creating new opportunities for data center development in markets that align with national and regional priorities. Operators are paying close attention to policy developments because regulatory support can influence long-term growth prospects.

The interaction between AI policy and infrastructure planning is likely to become even more significant in the coming years. Countries seeking to attract AI investment must ensure that energy resources, connectivity, and development frameworks support future demand. Infrastructure therefore occupies a central position within broader technology strategies. Europe’s evolving policy environment will continue shaping where capacity is built and how quickly new projects move forward.

The Rise of AI Inference Infrastructure

The Next Growth Phase May Be More Distributed

Much of the initial discussion surrounding AI infrastructure focused on training large models. These environments require extensive computing resources and often favor locations capable of providing large-scale power capacity. As AI adoption expands, however, attention is increasingly shifting toward inference workloads. Inference occurs when trained models process requests from users, applications, or automated systems. This activity is expected to represent a significant portion of future AI demand.

Inference workloads have different infrastructure requirements than training environments. While training clusters can often operate in remote locations optimized for energy availability, inference platforms frequently need to remain closer to users. Low latency is important for applications such as generative AI assistants, industrial automation systems, healthcare tools, and real-time analytics platforms. This requirement supports a more distributed infrastructure model in which computing resources are deployed across multiple regions.

The growth of inference infrastructure may create opportunities for a wider range of European markets. Cities and regions that were previously considered secondary locations could benefit from demand for localized AI services. This trend aligns with the broader diversification already occurring within the data center industry. Rather than concentrating all capacity within a handful of major hubs, future growth may be distributed across a larger network of interconnected markets. The expansion of inference infrastructure is therefore likely to influence Europe’s digital geography significantly.

Edge Infrastructure Gains Importance

The rise of inference workloads is also increasing interest in edge computing infrastructure. Edge facilities process data closer to where it is generated or consumed, reducing latency and improving responsiveness. AI applications often benefit from these characteristics because they support real-time decision-making and interactive user experiences. As organizations deploy AI across industries, demand for edge infrastructure is expected to grow. Europe’s diverse geography and population distribution make edge computing particularly relevant. Businesses and public-sector organizations increasingly require digital services that operate efficiently across multiple regions. Deploying infrastructure closer to users can improve performance while reducing reliance on centralized facilities. This approach complements rather than replaces traditional hyperscale environments. Both models are likely to coexist as part of a broader AI ecosystem.

The growing importance of edge infrastructure reinforces the trend toward geographic diversification. Markets that may not attract large training clusters could still play important roles within distributed inference networks. This creates new opportunities for regional infrastructure development. The next phase of Europe’s data center expansion may therefore involve a wider variety of facility types and deployment strategies than previous growth cycles.

What Europe’s Data Center Map Could Look Like by 2030

Growth Will Likely Be More Geographically Diverse

Europe’s future data center landscape is unlikely to mirror the concentration patterns that defined the cloud era. Traditional hubs will remain important because they possess extensive ecosystems, strong connectivity networks, and large customer bases. Frankfurt, London, Amsterdam, Paris, and Dublin are expected to continue serving as major centers of digital activity. Their role within the European economy remains too significant for rapid displacement.

Future growth, however, is increasingly likely to occur across a broader set of locations. Southern European markets such as Madrid and Milan are attracting attention because they offer opportunities for expansion and access to renewable energy resources. Nordic countries continue to benefit from their energy advantages and favorable environmental conditions. Eastern European markets are strengthening their positions as connectivity improves and investment increases. This combination of factors supports a more distributed infrastructure model.

The shift does not represent a transfer of dominance from one group of markets to another. Instead, it reflects the growing complexity of infrastructure requirements. Different workloads benefit from different operating environments. Training, inference, edge computing, and cloud services each possess unique characteristics that influence deployment decisions. The result is a data center ecosystem that may become more specialized and geographically diverse over time.

Energy Will Remain the Defining Variable

Among all the factors influencing Europe’s infrastructure evolution, energy appears likely to remain the most important. AI demand continues increasing the amount of electricity required to support digital services. Access to reliable, scalable, and sustainable energy resources will therefore play a central role in future site selection decisions. Markets capable of providing these resources may attract disproportionate levels of investment. The importance of energy extends beyond operational costs. Electricity availability directly affects development timelines, expansion potential, and long-term competitiveness. Regions with strong energy infrastructure possess advantages that are becoming increasingly valuable as demand grows. Policymakers, utilities, and infrastructure operators are all responding to this reality by prioritizing energy planning within broader digital strategies.

This trend suggests that the future map of Europe’s data center industry will be shaped as much by energy networks as by telecommunications infrastructure. Connectivity remains essential, but electricity is becoming equally important. Understanding this shift is critical for interpreting how the market is evolving. AI is changing not only where computing occurs but also the factors that determine where infrastructure can be built successfully.

Conclusion

Europe’s data center industry is entering a new phase defined by AI-driven demand, energy constraints, sustainability objectives, and evolving policy priorities. The factors that shaped infrastructure investment during the cloud era remain relevant, but they are no longer sufficient on their own. Power availability, renewable energy access, permitting efficiency, and digital sovereignty considerations are increasingly influencing where new capacity can be developed. These changes are reshaping the competitive landscape across the continent. Traditional hubs such as Frankfurt, London, Amsterdam, Paris, and Dublin continue to occupy central positions within Europe’s digital economy. Their connectivity ecosystems, enterprise presence, and infrastructure density ensure that they will remain important destinations for investment. At the same time, emerging markets are attracting greater attention as operators seek locations capable of supporting future growth. Southern Europe, the Nordics, and parts of Eastern Europe are benefiting from this shift as infrastructure requirements evolve.

Artificial intelligence is accelerating many of these changes because it places unprecedented demands on energy systems and computing environments. Training clusters, inference platforms, and distributed AI services each require different forms of infrastructure support. Meeting these needs is encouraging a more diversified development model that extends beyond traditional metropolitan centers. The next generation of infrastructure investment is therefore likely to be distributed across a broader range of regions and facility types.

Policy developments are reinforcing this transformation. Governments increasingly view digital infrastructure as a strategic asset connected to economic growth, innovation, and technological competitiveness. Sustainability regulations, AI initiatives, and digital sovereignty objectives are all influencing investment decisions. Infrastructure planning has become more closely linked to public policy than at any previous point in the industry’s history. The result is a European data center map that is gradually becoming more complex, more distributed, and more energy-focused. The continent’s leading markets are not disappearing, but they are being joined by a growing group of emerging locations with distinct advantages. AI is acting as the catalyst for this transition, reshaping how infrastructure is planned, financed, and deployed. By the end of the decade, Europe’s digital infrastructure landscape may look substantially different from the one that emerged during the first generation of cloud computing.