The AI infrastructure investment narrative has been dominated by the companies building facilities and buying hardware. The hyperscalers committing hundreds of billions. The private equity firms deploying permanent capital into data center operating companies. The neocloud operators racing to secure GPU fleets and power positions before the market tightens further. This framing is accurate as far as it goes, and it systematically misses the actors who actually hold the binding power over when any of those investments become operational. Those actors are the regulated utilities whose transmission and distribution infrastructure, interconnection queues, and generation expansion plans determine the fundamental timeline of the AI buildout, and they are transforming their commercial and regulatory strategies in response to AI infrastructure demand in ways that will define the terms of the industry’s next decade more than any GPU allocation or data center lease.

Utilities Are Entering a Historic Investment Cycle

More than 30 utilities cited data centers as a top growth driver in their Q1 2026 earnings reports, making AI the primary catalyst for the largest utility capital investment cycle in American history. US utilities plan $1.4 trillion in combined capital expenditure through 2030, covering new power plants, transmission lines, distribution networks, and grid hardening, primarily to serve data center load growth. Duke Energy leads with $102.2 billion planned through 2030, followed by Southern Company at $81.2 billion and American Electric Power at $72 billion. These are not infrastructure investments that utilities are making on speculative demand projections. They are investments driven by signed interconnection agreements, executed power purchase agreements, and committed load additions from hyperscalers and colocation operators whose capital commitments are as firm as any customer commitment a regulated utility has ever received.

The utilities are building for AI demand at a scale that is already the largest single driver of their capital programmes and that is making data center operators their most consequential customers.

The Rate Class Revolution That Changed the Commercial Relationship

The most significant structural change in the utility-data center relationship over the past 18 months is the proliferation of AI-specific rate classes that move data center operators from being large industrial customers under standard tariffs to being a distinct regulated customer category with its own cost allocation framework, interconnection timeline, and service terms. In November 2025, Virginia’s State Corporation Commission approved Dominion Energy’s request to create the GS-5 rate class for the largest electricity users, covering loads above 25 megawatts and designed specifically for data center customers. The GS-5 rate class includes demand guarantees covering generation and transmission, a 14-year contract term for large users, and a tariff structure that separates the cost of service for large electricity users from the cost of service for the residential and small business customers who share the grid.

The GS-5 rate class is not a favour to data center operators. It is a commercial structure that serves both parties: data center operators get the long-term price certainty and interconnection priority that they need to justify multi-year infrastructure investments, and Dominion gets the committed revenue and demand guarantee that allows it to finance the generation and transmission expansion that data center load growth requires without allocating all the construction risk to its regulated rate base. Dominion Energy currently serves approximately 450 data centers among its roughly 2.7 million total customers in Virginia, making data centers a customer category that represents a small fraction of customer count but a growing fraction of revenue and an overwhelming fraction of load growth.

How Utilities Are Restructuring Grid Economics

The rate class formalises that commercial reality by creating a structured service relationship that matches the economics of both the utility and the data center operator rather than forcing both into a tariff framework designed for a very different customer profile.

AEP Ohio created a data center tariff in July 2025 that requires financial commitments from developers before grid connections are approved, a model that other utilities are now studying and adapting. The AEP Ohio tariff requires data center developers to post financial assurance covering the cost of grid upgrades required for their connection, rather than socialising those costs across all ratepayers. That cost allocation mechanism is what Monitoring Analytics recommended in its Q1 2026 state of the market report, and it represents a fundamental shift in the commercial terms under which data centers access the grid.

The era when a data center developer could secure a grid connection on standard industrial tariff terms and distribute grid upgrade costs across the existing ratepayer base is ending state by state, utility by utility, as the political and regulatory pressure from ratepayers, consumer advocates, and utility commissions produces tariff structures that assign infrastructure costs to the loads that necessitate them.

The 14-Year Contract Model That Gives Utilities Structural Power

The long-term contract provisions embedded in the new AI-specific rate classes represent the most consequential commercial shift in the utility-data center relationship. A 14-year Dominion contract is not just a pricing arrangement. It is a commitment by the data center operator to take service from Dominion for 14 years, paying demand charges whether or not the facility is operational, and providing Dominion with the revenue certainty needed to finance the generation and transmission expansion the commitment requires. That revenue certainty converts the data center operator’s load commitment into a utility credit quality improvement that allows Dominion to finance infrastructure at lower cost than if it were financing against speculative demand projections.

The structural power that long-term AI contracts give utilities is the power of an indispensable counterparty. A data center developer who has executed a 14-year Dominion GS-5 contract has made an infrastructure decision that cannot be easily reversed. They are committed to a specific geographic location, a specific utility service territory, and a specific set of commercial terms for the life of the contract. The utility whose service territory captures a data center under a 14-year contract has a 14-year customer whose load growth, upgrade requests, and expansion plans will all route through the utility relationship. That customer concentration dynamic, multiplied across hundreds of data center customers, is transforming utilities from regulated commodity providers into strategic counterparties whose commercial decisions shape the geography, timeline, and economics of the AI buildout.

The Generation Partnership Model That Is Reshaping Utility Strategy

Beyond rate class innovation, utilities are developing new generation partnership models with data center operators that extend the commercial relationship from power delivery into power production. Dominion Energy and Amazon are collaborating on the advancement of Small Modular Reactor nuclear development in Virginia, a partnership that positions Dominion as both the generation developer and the grid operator for Amazon’s Virginia data center loads. The Tennessee Valley Authority has signed agreements for 6 gigawatts of small nuclear capacity linked to hyperscaler data center development commitments, creating a generation development pipeline that is justified by and financed against data center load commitments rather than speculative grid demand projections.

These generation partnership structures transform the utility from a passive infrastructure provider into an active participant in data center development economics. A utility that co-develops a nuclear or gas generation facility with a hyperscaler is bearing construction risk, technology risk, and regulatory risk in exchange for a share of the revenue that the generation asset produces over its operating life. The revenue share creates a direct financial alignment between the utility’s generation investment and the data center operator’s operational expansion that does not exist in the standard utility-customer tariff relationship. The utilities that have moved earliest and most aggressively into generation partnership structures with hyperscalers are building commercial relationships that compound over time as the hyperscalers’ data center load grows and the partnership framework extends naturally to each new generation of capacity addition.

The Equity Stake Model That Changes Utility Incentives

The most aggressive expression of the utility transformation is the acquisition of equity stakes in data center development projects or infrastructure vehicles alongside private capital. Brookfield’s $6 billion minority investment in Duke Energy Florida and KKR and PSP Investments’ joint investment in AEP’s Ohio and Indiana Michigan transmission companies are not utility-to-data center equity investments, but they are structural precedents for private capital taking equity stakes in utility infrastructure specifically to accelerate data center load service. The same logic that makes private capital want equity in utility transmission infrastructure applies in reverse to utilities that want equity exposure to the data center load growth that is driving their transmission expansion.

Some utilities are exploring direct equity participation in data center development vehicles as a mechanism for sharing in the economic value that their grid infrastructure creates rather than capturing value only through regulated tariff revenue. A utility that receives only regulated tariff revenue from a data center that contributes to a 400% PJM capacity market price increase is capturing a small fraction of the economic value its infrastructure enables. A utility with an equity stake in the data center development vehicle capturing that capacity market price increase is aligned with the data center operator’s commercial success rather than simply being a cost of service for it. The equity participation model is early-stage at most utilities, constrained by regulatory frameworks that limit the activities of regulated entities and by the risk appetite of utility management teams whose investor base values predictable regulated earnings over equity upside.

But equity participation offers compelling enough economics that utilities in states with flexible regulatory frameworks are actively evaluating it, and the precedents established in 2026 will shape the utility-data center commercial relationship for the next decade.

The AI Forecasting Capability That Is Becoming Utilities’ Most Valuable Asset

The transformation of US utilities into strategic AI infrastructure counterparties is producing an unexpected competitive asset: AI-driven load forecasting capability that no other actor in the AI infrastructure ecosystem can replicate. Utilities have load data covering every connection point in their service territory, historical consumption patterns for every customer class, weather correlation models that predict load variations across seasons and climate conditions, and generation dispatch models that optimise resource commitment across the real-time and day-ahead electricity markets. Applying machine learning to that data produces load forecasting capability that is orders of magnitude more accurate than the engineering-based forecasting models that utilities used a decade ago.

For AI infrastructure development, accurate utility load forecasting is commercially critical because it determines which interconnection requests receive queue priority based on system impact, which transmission upgrades utilities fund based on projected load growth, and which grid expansion investments utilities approve based on the likelihood that projected demand materialises. US utility data center power supply is expected to jump 22% in 2025 to 61.8 gigawatts and reach 134.4 gigawatts by 2030, according to S&P Global. Forecasting whether that trajectory is accurate or whether specific regional markets will experience faster or slower growth requires exactly the data-driven load forecasting capability that utilities have built over decades.

The utility that can tell a data center developer with confidence that its service territory can absorb 500 megawatts of new load in 2027 without reliability risk, or that the developer’s preferred site will require a $400 million transmission upgrade that will take four years to complete, has information that is unavailable to any other actor in the development process. That informational advantage makes the utility the indispensable counterparty at the point in the development process where data center investments succeed or fail.

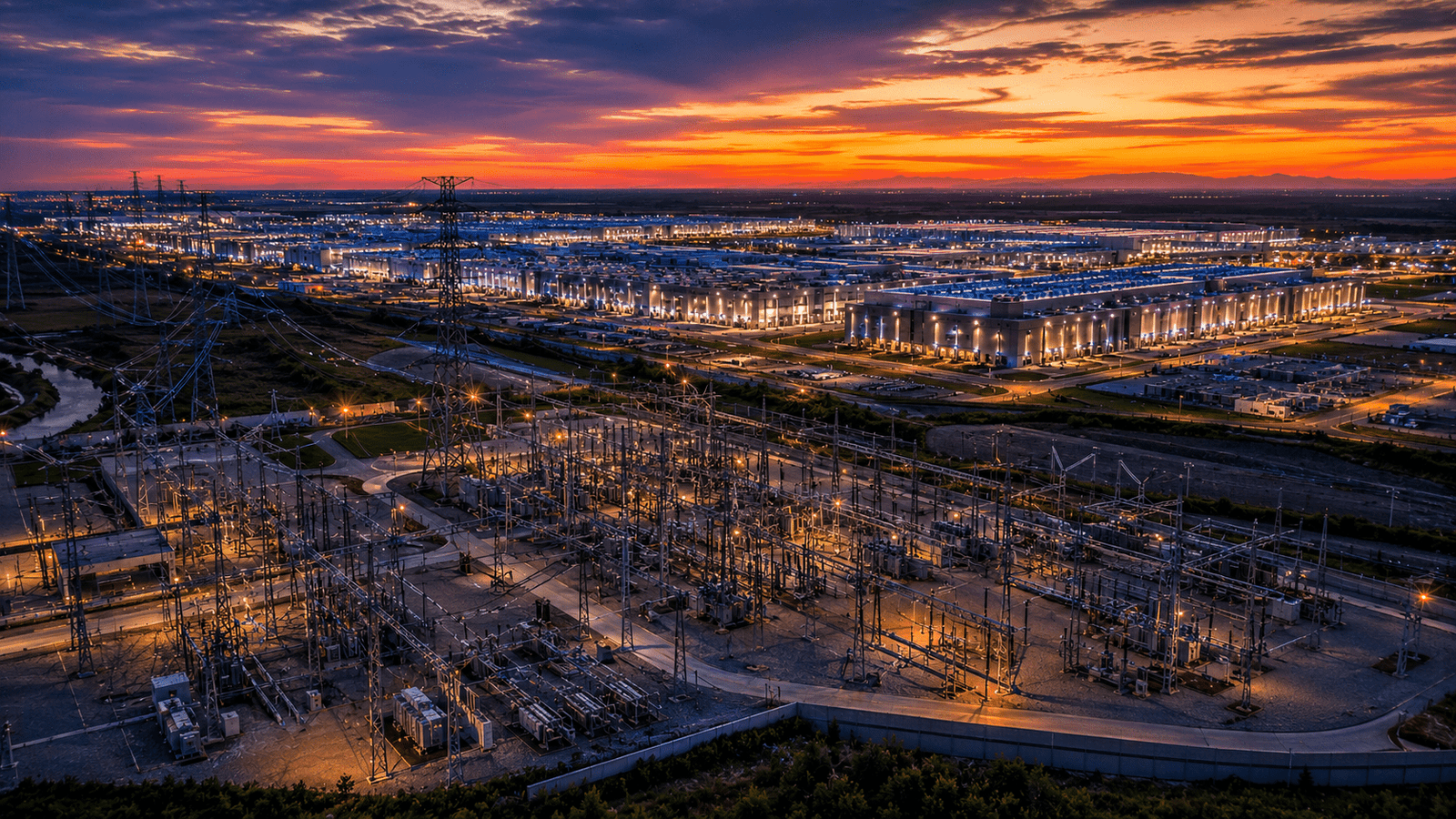

The Transmission Investment That Determines Who Wins the Buildout

The utility transformation that receives the least attention in AI infrastructure analysis is the most consequential for determining which markets will have the operational data center capacity the buildout requires. Transmission infrastructure investment is the mechanism through which utilities convert the theoretical capacity of their generation fleet into the operational capacity to serve new large loads. A service territory with abundant generation but insufficient transmission to deliver that power to a data center campus is a service territory whose generation capacity cannot serve the campus regardless of how much the developer is willing to pay.

Transmission upgrades are the longest-lead-time items in the utility infrastructure stack, typically requiring three to seven years from planning approval to operational service, and the utilities whose transmission expansion programmes are most advanced relative to anticipated data center load are the utilities whose service territories will capture the most AI infrastructure investment over the next five years.

Dominion Energy’s 2024 resource plan projects nearly 27 gigawatts of new generation by 2039, including 21 gigawatts of renewable energy and 5.9 gigawatts of gas, supported by a transmission expansion programme that is designed to deliver that generation to the Northern Virginia data center corridor that already hosts the highest concentration of data center load in the world. The transmission investment is both the most capital-intensive component of Dominion’s resource plan and the most strategically significant, because the data center developers who commit to Dominion’s service territory are betting that Dominion’s transmission expansion will deliver the capacity they need on the timelines the resource plan projects.

Why Transmission Timelines Matter

A transmission upgrade that runs six months late delays the data center’s go-live date regardless of whether the facility construction, GPU procurement, and customer contracts are all on schedule. The transmission timeline is the binding constraint on data center delivery in every market where transmission is the capacity constraint, which is most of the markets that the AI buildout is most actively pursuing.

The utilities that have secured regulatory approval for their transmission expansion programmes and that can provide data center developers with firm delivery timelines and committed interconnection dates are in a fundamentally stronger commercial position than utilities that are still navigating the approval process. Combined with increases already implemented since 2021, consumer electricity bills have risen approximately 40%, with further increases expected as utilities file new rate cases to recover capital investments through 2030. The utilities that have structured their rate recovery to assign AI infrastructure costs to AI infrastructure customers rather than to residential ratepayers are building political durability alongside physical infrastructure durability, creating the conditions for sustained investment at AI infrastructure pace rather than one-off expansions that generate political backlash before the next approval cycle.

The Rate Recovery That Funds the Buildout

The utility’s ability to fund the transmission and generation expansion that AI infrastructure requires depends on its ability to recover the cost of that investment through regulated rates. Rate recovery determines how utilities distribute infrastructure investment costs across their customer base, and its structure, including how quickly utilities can earn returns on investment, how much cost they assign to data center customers versus the broader rate base, and which regulatory process governs new rate case approvals, determines whether utilities can expand AI infrastructure at the pace hyperscalers require.

Dominion proposed its first base-rate increase since 1992 in February 2025, adding approximately $8.51 per month in 2026 and $2.00 per month in 2027 for residential customers in Virginia, directly attributable to the generation and transmission expansion needed to serve data center load growth. That rate increase is the manifestation, in the residential customer’s monthly bill, of the transmission investment that makes the Northern Virginia data center ecosystem commercially viable. The political tension between residential ratepayers bearing cost increases and hyperscalers benefiting from the infrastructure those increases fund is the same tension that produced Florida’s SB 484 and Monitoring Analytics’ recommendation that data centers bring their own power.

The utilities navigating that political tension most effectively are those that have developed AI-specific rate classes which assign infrastructure costs to data center customers before the costs appear in residential bills, rather than after the political pressure from residential ratepayer groups has already accumulated. The AEP Ohio data center tariff shows how utilities can scale AI infrastructure development while managing the political risks of appearing to prioritise hyperscaler demand over residential ratepayer protection.

The Competitive Differentiation That Is Emerging Between Utility Service Territories

The transformation of utilities into strategic AI infrastructure counterparties is producing competitive differentiation between utility service territories that did not exist five years ago and that is becoming one of the most important factors in data center site selection. A utility service territory with an AI-specific rate class offering 14-year contracts, an approved transmission expansion programme with firm delivery timelines, a generation partnership framework with major hyperscalers, and a track record of delivering interconnection agreements on committed timelines is a fundamentally more attractive data center development environment than a service territory whose utility is still processing data center load through standard industrial tariffs on interconnection queues designed for conventional commercial and industrial customers.

That differentiation is already showing up in capital allocation patterns. Virginia’s Loudoun County, served by Dominion Energy, remains the epicenter of the global data center industry, not only because of its historical concentration of data centers and internet exchange points but because Dominion’s AI-specific rate class infrastructure, transmission expansion programme, and regulatory engagement have made it the utility service territory best equipped to serve hyperscaler-scale AI infrastructure development. Counties adjacent to Loudoun whose utilities have developed less mature AI infrastructure programmes are attracting data center development at only a fraction of Loudoun’s pace despite offering comparable land, water, and power generation resources. The utility’s commercial and regulatory programme is the differentiating factor, and the utilities that are investing in developing those programmes are building moats that will compound as AI infrastructure investment concentrates in the service territories with the most developed utility capabilities.

The Utility as Grid Stability Asset

The final dimension of the utility transformation that has direct commercial significance for AI infrastructure development is the emerging role of large data center loads as grid stability assets rather than simply grid stability challenges. Utilities are beginning to develop demand response programmes specifically designed for data center customers, allowing data centers to reduce load during grid stress events in exchange for rate credits or capacity market revenue. Data centers are poised to become a key stabilising force in the energy transition when utilities are rewarded for collaboration rather than protecting reserved capacity, and when data centers can drive grid expansion through storage and on-site generation investment.

A data center that can respond to a utility request to reduce load by 50 megawatts within five minutes is providing a grid balancing service that has commercial value to the utility and that, when priced appropriately through demand response programmes, reduces the net cost of grid service for the data center operator.

Why AI Inference Workloads Matter

The AI inference workload characteristics that make data centers good demand response candidates are the same characteristics that make them challenging grid customers in other respects. Inference workloads offer more flexibility than training workloads in their moment-to-moment power draw because operators can briefly delay inference requests or route them to lower-power hardware configurations during demand response events without risking the job failures that often disrupt training runs. A data center that can defer inference requests by 30 to 60 seconds during a demand response event can participate in utility demand response programmes without material impact on the user experience of the applications running on its infrastructure.

That capability, once developed and commercialised, transforms the data center from a passive grid load into an active grid asset whose demand flexibility has monetary value to the utility and, through the utility, to every other customer on the grid. The utilities that develop the commercial frameworks for pricing and contracting data center demand response will have an additional tool for managing the grid reliability impacts of data center load growth that the current policy and commercial conversation around AI infrastructure has not yet fully incorporated.

What This Means for AI Infrastructure Strategy

The transformation of US utilities into strategic AI infrastructure counterparties has direct implications for how data center developers, hyperscalers, and infrastructure investors should think about their utility relationships. The era when utilities operated as commodity providers with regulator-defined service terms and commercially distant relationships managed by energy procurement teams is ending. The utilities that are developing AI-specific rate classes, building generation partnership models with hyperscalers, and acquiring the load forecasting capability needed to make commitments against AI infrastructure demand are becoming strategic partners whose cooperation is as consequential for data center development success as GPU procurement or capital access.

Data center developers who treat their utility relationships as transactional will find that the utilities with the strongest AI infrastructure positions are increasingly willing to prioritise developers who engage them as strategic partners over those who engage them as commodity providers. A utility that has 500 megawatts of interconnection capacity available in 2027 and receives requests from ten developers can allocate that capacity to the developers whose long-term committed load, generation co-investment, and regulatory engagement make them the most valuable long-term customers rather than to the developers who simply filed their interconnection requests earliest. The developers who understand that the utility relationship is a source of competitive advantage, not a procurement category, are the ones building the positions in the AI infrastructure market that will matter most when grid constraints become the binding constraint on buildout pace for every other developer in the market.

The Utilities Defining the Next Phase of AI Infrastructure

The US electricity market not being built for AI documented that the regulatory frameworks are changing to reflect this new reality. The commercial strategies of the utilities operating within those frameworks are changing faster than the regulatory frameworks themselves, and the AI infrastructure market that understands and engages with those commercial strategies earliest will build the most durable grid positions in the buildout.

The utilities who emerge from the current AI infrastructure cycle as the most valuable counterparties will be those who recognised earliest that their position in the AI buildout was not merely operational but strategic. The regulated utility that owns the transmission infrastructure, the generation capacity, the interconnection queue authority, and the rate-setting power that governs when and at what cost AI data centers access the grid is not simply a vendor in the AI infrastructure supply chain. It is the institution that determines whether the supply chain delivers at all. The hyperscalers, private equity firms, and neocloud operators who are investing hundreds of billions of dollars in AI infrastructure on the assumption that the grid will accommodate their ambitions are investing on the utilities’ terms whether they have articulated it that way or not.

Utilities that proactively define those terms through AI-specific rate classes, long-term generation partnerships, and strategic equity participation will capture the most durable value from the buildout. Utilities that continue using legacy commercial frameworks for AI infrastructure requests will react too slowly to a transformation that has already reshaped the service territories leading the AI infrastructure buildout.