The liquid cooling market has never moved faster or been harder to navigate. In the six months between November 2025 and April 2026, the sector saw six major acquisitions that collectively reshaped the competitive landscape: Eaton acquired Boyd Thermal for $9.5 billion in November 2025, Daikin Applied acquired Chilldyne in November 2025, Trane Technologies acquired LiquidStack in February 2026, Ecolab acquired CoolIT Systems from KKR for $4.75 billion in March 2026, Vertiv acquired ThermoKey in March 2026, and Vertiv acquired Strategic Thermal Labs in April 2026. The pace of consolidation signals genuine urgency: established industrial players and infrastructure vendors are paying premium prices, Ecolab paid 29 times next-twelve-months EBITDA for CoolIT, to secure positions in a liquid cooling market they believe will become mandatory infrastructure for every serious AI data center within three years.

The consolidation has not simplified the operator’s procurement decision. It has changed who the vendors are, expanded the capabilities of the largest players, and accelerated the migration of independent specialists into larger corporate structures. But it has not produced the common standards, interoperability frameworks, or vendor-neutral evaluation criteria that would allow an operator building a new AI data center campus today to make a confident, well-informed liquid cooling procurement decision with reasonable certainty that the choice will remain technically and commercially viable for the ten to fifteen year life of the facility.

Operators Still Face a Fragmented Vendor Ecosystem

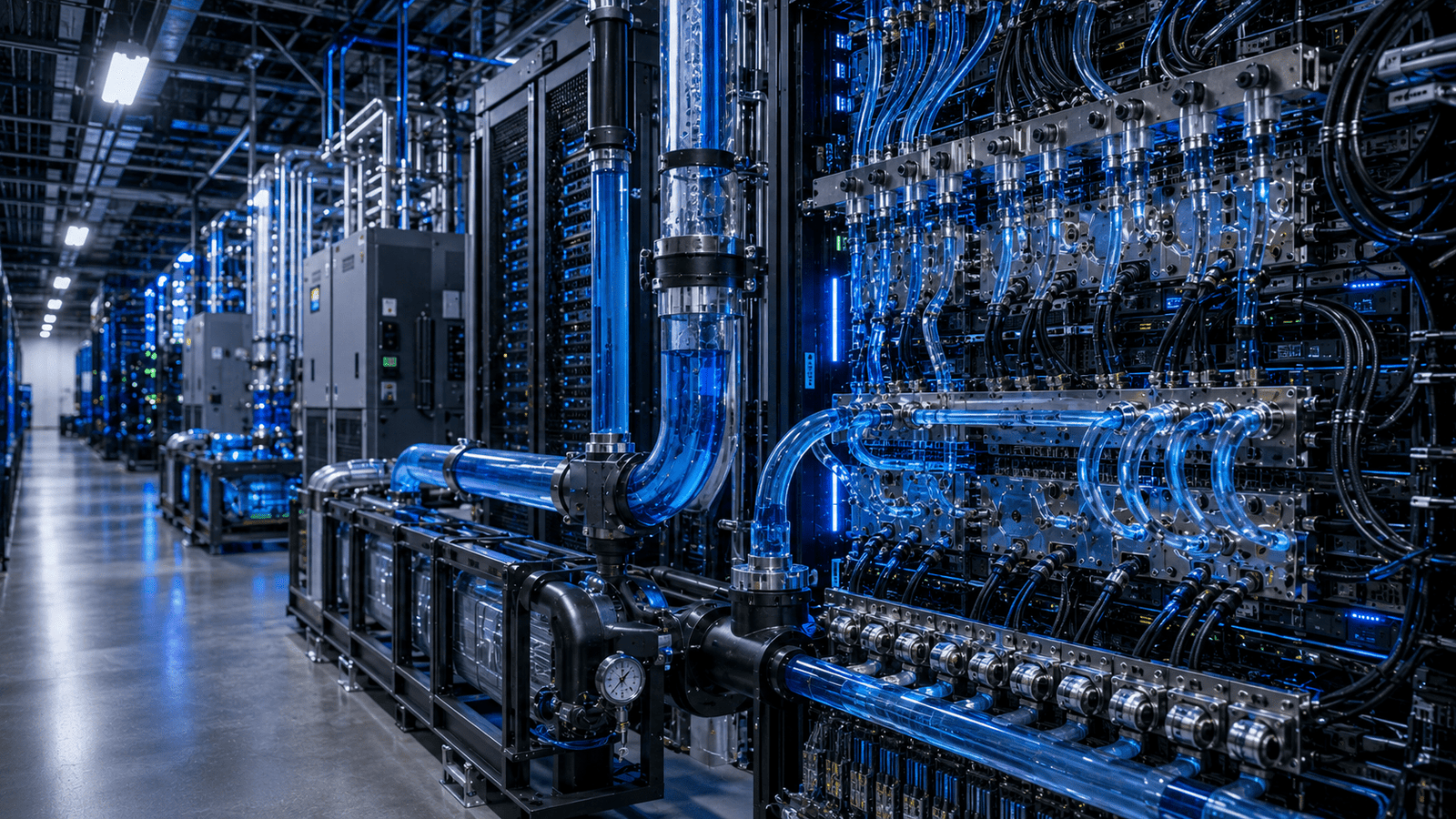

The operator who must choose between direct liquid cooling from Vertiv, Schneider Electric, Ecolab–CoolIT, nVent, Rittal, Submer, Asetek, LiquidStack, or Asperitas today is choosing between systems with different fluid types, different operating pressures, different manifold interfaces, different monitoring and control architectures, and different maintenance requirements. The vendor landscape has fifteen-plus active players and no common standard governing how their systems interconnect, what fluid chemistry they require, or how their monitoring data integrates with data center infrastructure management platforms.

The M&A-Driven Market Shift

The six acquisitions of the past six months each followed a recognisable strategic logic. Eaton acquired Boyd Thermal to add liquid cooling hardware to a power management portfolio whose customers were asking for integrated power-and-cooling solutions. Ecolab acquired CoolIT to transform itself from a water treatment and monitoring services company into a comprehensive cooling platform with existing relationships across more than 1,000 data centers. Vertiv acquired ThermoKey to strengthen its heat rejection portfolio and Strategic Thermal Labs to deepen its engineering capability at the interface between server-side liquid cooling and data center infrastructure. Each acquirer was rational.

The cumulative effect is a market where the top tier now consists of large, well-capitalised platform vendors whose liquid cooling capabilities extend across hardware, chemistry, monitoring, and services, while the mid-tier and lower tier consist of independent specialists and startup-stage innovators whose differentiated technology may or may not survive as standalone commercial entities as the major platforms expand their capabilities.

The operator problem is that the acquisition activity is ongoing and its trajectory is not yet settled. Trane Technologies acquiring LiquidStack and Daikin acquiring Chilldyne are signals that large HVAC and industrial cooling companies are entering the data center liquid cooling market through acquisition, bringing capital, distribution, and service infrastructure but not necessarily the deep data center operational expertise that liquid cooling at AI density requires. An operator who selects a mid-tier liquid cooling vendor today on the basis of its technology performance and price may find within 18 months that the vendor has been acquired and its product roadmap, support structure, and commercial terms have changed as a result. The acquisition risk is a real procurement consideration that the operator decision framework must account for alongside the technical evaluation.

The Standards Gap That Makes Every Decision a Bet

The liquid cooling vendor market’s most significant structural problem for operators is the absence of common standards governing the interfaces, fluid chemistry, and monitoring architectures of competing systems. In 2023, a high-density rack was 30 kilowatts; by 2026 deployments regularly push 240 kilowatts per rack, with some experimental designs surpassing 1 megawatt. The speed of that density increase has outrun the standards development process that normally produces the common specifications allowing different vendors’ equipment to interoperate reliably in complex facility environments. The result is a market where each vendor designs its liquid cooling system around proprietary manifold connections, preferred fluid chemistry, and control architecture, locking facility operators into that vendor’s product roadmap once installation is complete.

The lack of standards creates two specific risks for operators making liquid cooling procurement decisions today. The first is vendor lock-in: once a facility is designed and built around a specific vendor’s CDU architecture, manifold specifications, and fluid chemistry, switching to a different vendor’s system requires structural changes to the facility that are prohibitively expensive without a major renovation. The second is specification risk: the server-side cooling specifications that GPU manufacturers including Nvidia publish for their current hardware generation may change with the next generation in ways that are incompatible with the cooling infrastructure already installed, requiring the operator to either upgrade the cooling infrastructure mid-facility-life or accept hardware constraints imposed by the existing cooling system.

Vertiv’s acquisition of Strategic Thermal Labs was explicitly motivated by the need to deepen engineering capability at the interface between server-side liquid cooling and data center infrastructure, acknowledging that this interface is where the specification risk is most acute and where operator facilities are most vulnerable to incompatibility as hardware generations change.

What Operators Must Do Before Committing

The liquid cooling procurement decision is one of the most consequential and least reversible infrastructure choices an AI data center operator makes. The facility design, the floor loading, the plumbing infrastructure, and the monitoring systems are all shaped by the liquid cooling choice in ways that constrain every subsequent infrastructure decision for the facility’s life. An operator who makes this decision on the basis of current price-performance comparisons without adequately evaluating vendor stability, roadmap compatibility, standards participation, and acquisition risk is making a ten to fifteen year commitment on the basis of a two to three year vendor evaluation.

The operators navigating this market most effectively are treating liquid cooling procurement as a platform selection rather than a component purchase. They are evaluating vendors not just on the technical performance of their current products but on their participation in open standards bodies including the Open Compute Project and ASHRAE, their roadmap commitments for future GPU generations, their financial stability and M&A risk profile, and the interoperability of their monitoring and control systems with the data center infrastructure management platforms the operator already uses. An operator who selects a liquid cooling vendor based on those criteria, rather than purely on current hardware performance and pricing, is making a facility design decision that has a reasonable probability of remaining technically and commercially viable through the first hardware refresh cycle rather than requiring a costly mid-life intervention.

Why Standards and Interoperability Matter

The AI infrastructure buildout creating a supply chain crisis nobody planned for documented that the physical infrastructure decisions that data center operators make today determine the operational options available to them for a decade. The liquid cooling vendor choice is among the most permanent of those decisions, and the current market gives operators fewer reliable anchors for making that decision well than the scale of capital commitments should allow.

The standards landscape is slowly improving. The Open Compute Project’s Cooling Workgroup has produced initial specifications for coolant loop interfaces that several vendors have committed to supporting. ASHRAE TC 9.9 has updated its thermal guidelines to address AI-density workloads. The Green Grid has published guidance on water usage effectiveness metrics that are beginning to inform liquid cooling procurement conversations. None of these standards bodies have produced the binding interoperability specifications that would allow operators to mix vendors’ equipment within a single cooling loop, but the trajectory of standards development is toward greater interoperability rather than deeper fragmentation.

The operators who engage with the standards process now, by participating in OCP working groups, contributing to ASHRAE technical committees, and requiring vendors to demonstrate standards compliance in their procurement processes, are both accelerating the development of the standards ecosystem and creating the evaluation criteria that will make their next facility’s liquid cooling procurement decision meaningfully better informed than the one they are making today.