The investment narrative around AI has been constructed almost entirely around software and silicon. The companies that design the best models, build the fastest chips, and deploy the most capable cloud services are the companies that will capture the value of the AI transition. That narrative is not wrong. It is incomplete in a way that Goldman Sachs Alternatives, which manages more than $625 billion in alternative assets, believes is creating systematic mispricing across the AI investment landscape. In a new investment perspectives paper, Goldman argues that the companies capturing roughly 90% of AI profits today, chip designers, memory manufacturers, and semiconductor fabs, represent none of the physical bottlenecks that will determine whether artificial intelligence can actually scale.

Power generation, grid infrastructure, high-voltage components, advanced cooling, and mission-critical services collectively account for approximately 10% of AI-related earnings. They account for 100% of the chokepoints. The paper’s co-authors, Leonard Seevers, Jason Tofsky, and Sydney McConathy, state the investment implication directly: many investors are still looking to replicate past successes in data centers, missing the critical chokepoints that will define the next phase of growth.

Why Goldman’s Timing Matters

The timing of Goldman’s analysis matters. It arrives as the AI infrastructure buildout has accelerated to a pace where the physical constraints the paper identifies are no longer theoretical. The US faces a projected 45-gigawatt power shortfall for data centers by 2028, with 72 gigawatts of new capacity needed through 2030, the equivalent of 72 large nuclear power plants built in four years. Construction spending on data centers in the US has tripled over the last three years. Occupancy at third-party leased facilities remains near record highs. Vacancy rates are at record lows. Planned developments now total more than 50 million square feet, double the volume of five years ago.

Goldman has raised its data center power demand forecast multiple times, from 165% growth by 2030 versus 2023 levels, to 175%, to 220% in its most recent revision. Each revision reflects not a change in the demand model but a change in the investment behaviour of the largest buyers, whose reinvestment at scale steepens the power curve faster than prior estimates anticipated.

The Agentic AI Transition That Sharpens the Constraint

Goldman’s analysis identifies the transition to agentic AI as the force that transforms an already acute physical constraint into a defining strategic variable. Agentic AI systems, autonomous and always-on rather than episodic and prompt-driven, generate fundamentally different infrastructure demand from the chatbot and copilot applications that have characterised AI deployment to date. Agents use four times more compute tokens than chat applications, and multi-agent systems use 15 times more. Goldman Sachs projects that agentic AI will drive more than 90% of future demand for digital infrastructure, making current spending not a speculative bubble but a structural race to address physical constraints that are already binding.

The implication is that the data center infrastructure being built today is not adequate for the AI workloads that will run on it within three to five years. An infrastructure investment programme sized for current chatbot and inference workloads will be structurally undersized for agentic AI systems running continuously across enterprise workflows at 15 times the compute intensity. The developers and operators who are designing for agentic AI demand today, rather than for current workload profiles, are building infrastructure that will remain strategically valuable through the agentic transition. Those who are designing for current demand are building infrastructure that will face the same retrofit pressure that conventional data centers are already experiencing as GPU density requirements have exceeded the specifications of facilities designed just three years ago.

The rack density threshold forcing a rethink of every data center standard documented how quickly infrastructure assumptions become obsolete in the current cycle. The agentic AI transition is the next version of the same dynamic, operating at a larger scale and over a longer timeline.

The Six Forces Goldman Says Will Shape the Outcome

Goldman’s investment perspectives paper identifies six forces that will determine whether the AI infrastructure buildout generates the returns that current capital commitment levels require. The first is AI pervasiveness, the breadth of enterprise and consumer adoption that creates the demand base the infrastructure is sized to serve. The second is server and compute productivity, specifically how much useful work future hardware generations deliver per dollar of capital expenditure compared to current systems. The third is electricity prices, which Goldman identifies as a key variable because new natural gas plants take five to seven years to come online and renewables provide only intermittent power, making the energy cost trajectory of AI infrastructure highly sensitive to policy decisions and grid investment timelines that are outside operators’ direct control.

The fourth force is policy initiatives, covering regulatory frameworks, permitting reform, grid modernisation investment, and the evolving treatment of data center cost allocation by state utility commissions. Florida’s SB 484, signed May 7, is a direct example of policy initiative shaping infrastructure economics in a way that financial models built before the law did not anticipate. The fifth force is parts availability, covering the transformer, switchgear, optical connectivity, and advanced cooling component supply chains whose lead times have extended to five years in some categories and whose availability now governs delivery timelines more than capital commitment does.

The sixth force is people availability, with Goldman Sachs estimating that the industry will need approximately 760,000 additional power and grid workers by 2030, including 207,000 specialised transmission and distribution roles that require three to four years of training. The human capital constraint may prove harder to resolve than the hardware constraint because training a licensed electrician takes longer than building a transformer factory.

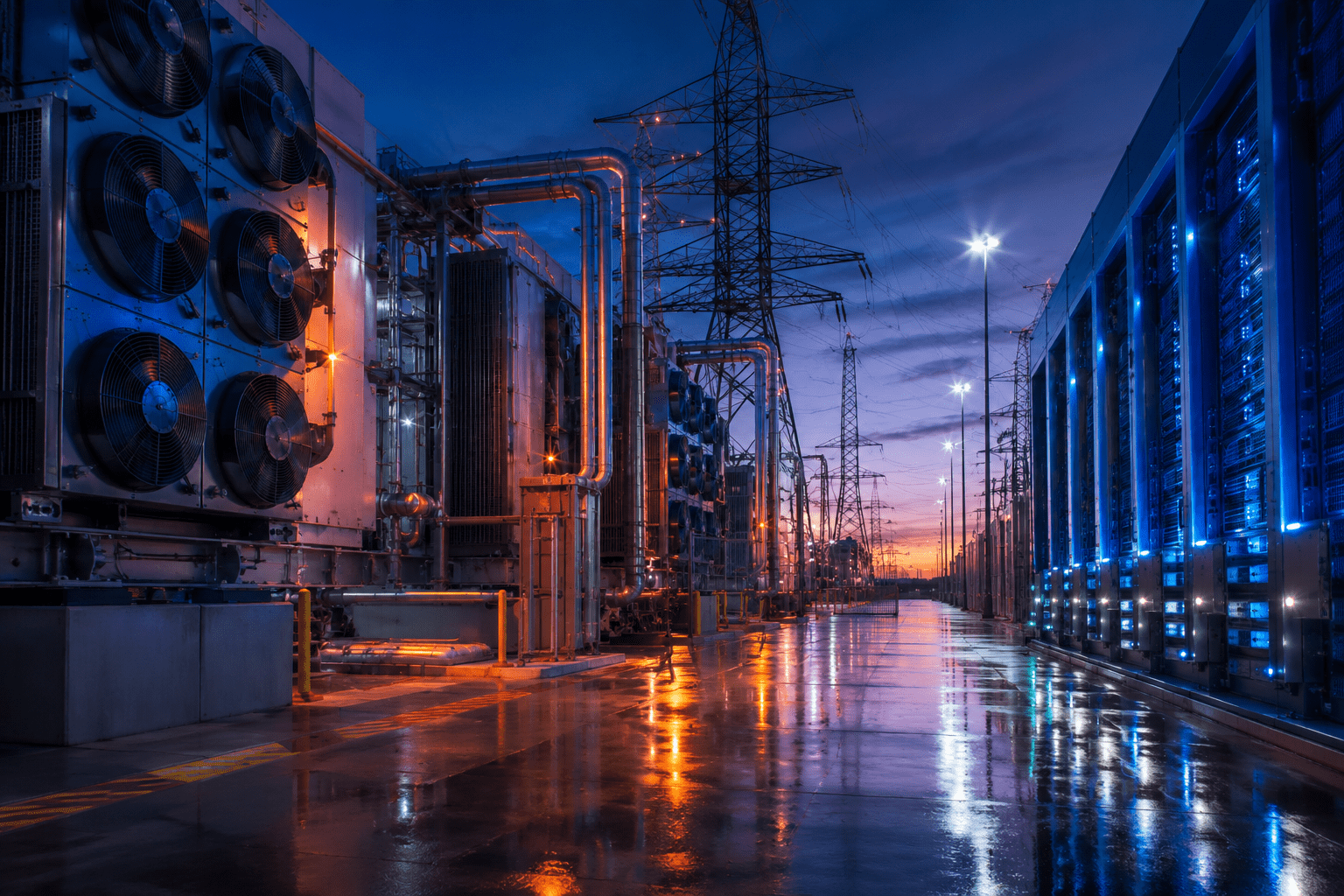

The Copper Wall Thesis and Its Investment Implications

Goldman’s most specific investment thesis in the paper is what it describes as the copper wall, a reference to the physical infrastructure layer of optical connectivity, cooling systems, and transformers that represents the true chokepoint in the AI buildout. Optics, cooling, and transformers are not generic inputs in this environment; they are chokepoints with pricing power. When vacancy is low, the development pipeline is full, and power connections are scarce, vendors with constrained capacity can defend margins in ways that commodity suppliers cannot. The copper wall thesis is an argument that the companies holding scarce pieces of the physical supply chain are pricing makers rather than pricing takers, and that the investment returns in the AI era will accrue disproportionately to those scarce physical asset holders rather than to the software and silicon layer that captures most of the current analytical attention.

The Nvidia-Corning Deal as a Real-World Example

The Nvidia-Corning partnership announced May 6, in which Corning will increase US optical connectivity manufacturing capacity by 10 times and Nvidia received the right to invest up to $3.2 billion in Corning stock, is the clearest recent expression of Goldman’s copper wall thesis playing out in real transactions. Nvidia is not investing $3.2 billion in Corning because optical fiber is a commodity. It is investing because optical connectivity is a chokepoint whose scarcity limits how quickly Nvidia’s own GPU hardware can be deployed at scale. The equity warrant aligns Nvidia’s financial interests with Corning’s manufacturing expansion in the same way that Goldman’s investment thesis aligns return expectations with the physical constraint layer rather than the profit-capturing layer.

The companies that understood the copper wall thesis earliest are already building the positions that Goldman’s paper argues the broader investment community is only now beginning to price. On Goldman’s analysis, the infrastructure layer that most investors treat as background to the AI story is actually the foreground where companies will build and defend the AI era’s most durable competitive advantages.

Why the Physical Infrastructure Layer Matters Most

That convergence between Goldman’s investment thesis and the operational reality playing out across AI infrastructure supply chains is the most important signal in the paper. The physical constraints Goldman identifies are not risks to be managed through hedging or diversification. They are structural features of the current AI buildout cycle that determine which operators can deliver capacity on commercially viable timelines and which cannot. The investment community that prices AI through the software and silicon lens alone is systematically undervaluing the physical infrastructure layer that makes everything above it possible. Goldman’s paper is an argument that the market is making that mistake at scale, and that the correction, when it comes, will benefit the operators and investors who understood the copper wall thesis before it became consensus.