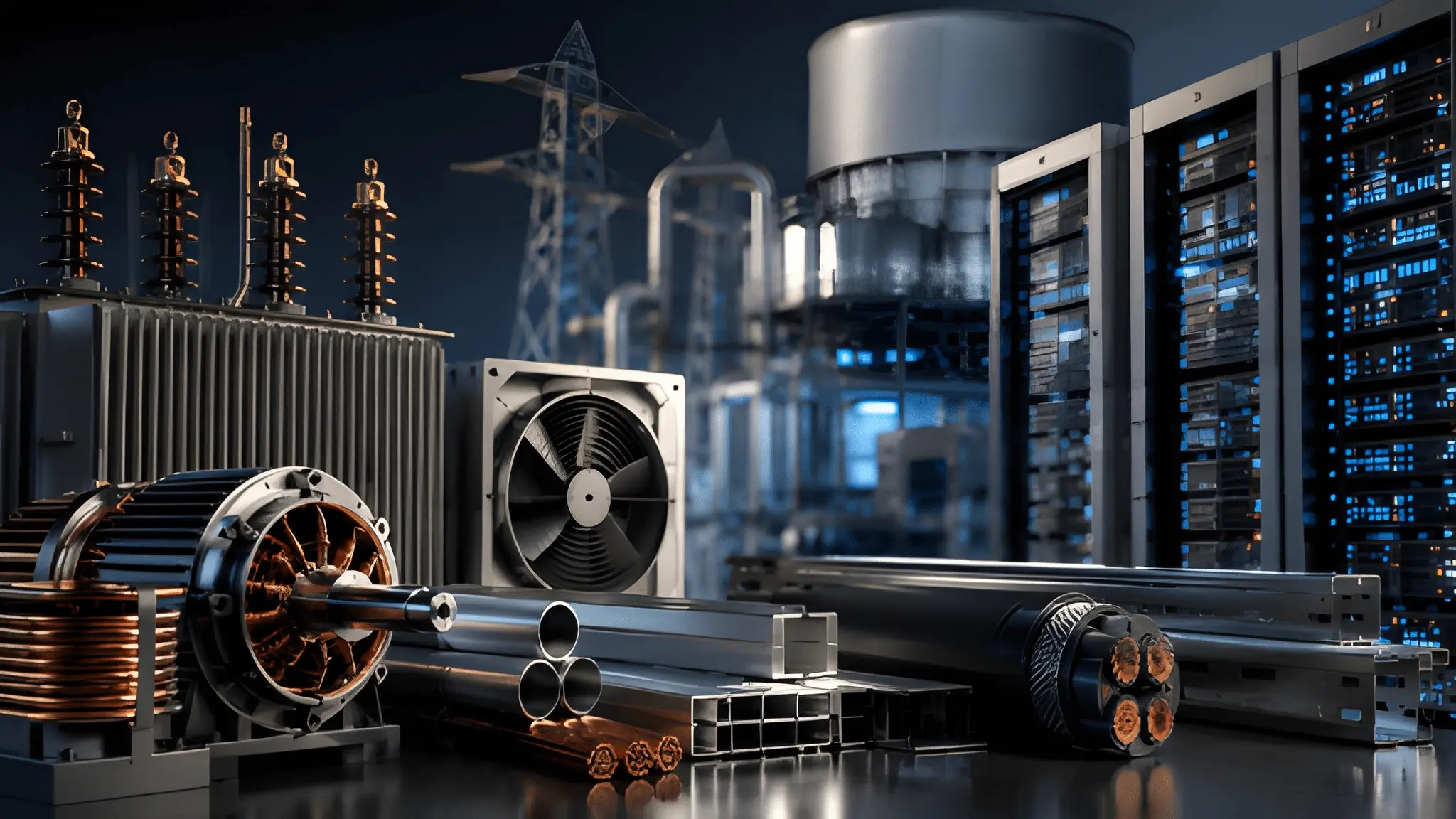

The market still treats artificial intelligence like a software spectacle. Investors chase chatbot launches, GPU shortages, model benchmarks and trillion-dollar valuations tied to cloud platforms. Yet the physical reality of AI looks far less glamorous. Every large language model ultimately depends on electricity, cooling capacity, transformers, cables, switchgear, backup power systems and industrial-scale engineering.

That shift is quietly redrawing the map of who benefits from the AI economy. The beneficiaries of the AI expansion are extending beyond software firms and hyperscalers into the industrial supply chain supporting data centre growth. In India, that shift is drawing greater market attention toward engineering manufacturers traditionally associated with power infrastructure and industrial capital expenditure cycles.

The AI narrative may still belong to chipmakers and cloud providers. The cash flows increasingly belong to whoever can keep data centres alive. That distinction matters because the economics of AI have changed. The first phase of the AI boom rewarded intelligence creation. The next phase appears set to reward infrastructure survival.

The AI Economy Has Become an Energy Economy

Modern AI systems consume enormous amounts of power. Training advanced models requires dense clusters of GPUs operating continuously across massive facilities. Inferencing at scale pushes electricity consumption even higher as adoption widens. That reality has triggered an infrastructure scramble stretching far beyond semiconductor manufacturing.

Data centre operators now compete for grid access, cooling efficiency and power reliability with the same intensity once reserved for computing performance. In many global markets, electricity availability has become a bigger bottleneck than land acquisition. Cooling systems have evolved into strategic assets rather than operational afterthoughts.

The industrial implications are enormous. Every new hyperscale facility requires transformers, high-voltage cables, switchgear, cooling units, precision HVAC systems, battery storage, diesel backup systems and advanced electrical engineering. AI infrastructure increasingly resembles a heavy industrial ecosystem rather than a purely digital one. This transition has created a structural opportunity for India’s engineering sector.

India Is Quietly Becoming AI’s Industrial Workshop

India may not yet dominate frontier AI models, but its engineering and manufacturing ecosystem is becoming increasingly relevant to the infrastructure supporting global AI expansion. That distinction often escapes mainstream market narratives. India’s industrial ecosystem supports manufacturing across electrical equipment, power transmission systems, industrial cooling and engineering services. As global data centre construction accelerates, those capabilities are attracting increased strategic and investor attention.

Companies once associated with routine infrastructure spending now find themselves exposed to one of the world’s fastest-growing capital expenditure cycles. The transformation is subtle but significant. Cable manufacturers are seeing demand tied to high-density power transmission. Transformer suppliers benefit from expanding grid connectivity requirements.

HVAC and cooling firms increasingly support high-performance computing environments where thermal management determines operational efficiency. Switchgear manufacturers sit directly inside the power distribution architecture required for AI facilities. None of these sectors traditionally generated excitement in technology investing circles. That may explain why much of the market still overlooks them. The AI boom has effectively turned industrial plumbing into strategic technology infrastructure.

Investors Still Prefer the Fantasy Version of AI

Markets often reward the most visible layer of technological disruption while ignoring the machinery underneath it. That pattern is repeating in AI. The attention economy surrounding artificial intelligence still revolves around consumer-facing applications, breakthrough models and semiconductor dominance. Those narratives are easier to market. Industrial supply chains rarely generate the same excitement as chatbots capable of writing essays or generating images.

Yet physical economics tells a different story. AI data centres cannot scale without uninterrupted power flow and thermal stability. Compute expansion depends on industrial capacity as much as software innovation. In some regions, utilities and engineering constraints now dictate the pace of AI deployment more than computing ambition itself.

That creates an unusual contradiction inside capital markets. Several AI-linked industrial businesses continue to be viewed primarily through the lens of cyclical manufacturing and infrastructure spending rather than as long-term enablers of digital infrastructure expansion. The result is a widening disconnect between narrative value and infrastructure value.

AI Is Reviving the Industrial Economy Nobody Wanted to Talk About

The AI era was initially framed as a triumph of software over traditional industry. Automation, cloud computing and digital platforms appeared to weaken the relevance of manufacturing-heavy sectors. Instead, AI may be reviving them. Industrial companies traditionally viewed as slow-growth businesses are gaining greater relevance within the expanding global compute infrastructure ecosystem. Electrical engineering, thermal management and power equipment manufacturing suddenly carry geopolitical and economic significance. The symbolism is striking.

The same market environment that celebrated asset-light digital platforms now depends on factories, copper networks, cooling technologies and industrial hardware. AI has not eliminated physical infrastructure. It has intensified dependence on it. That shift is particularly important for India because it aligns with the country’s manufacturing ambitions.

India’s role in the AI economy may evolve less through consumer applications and more through infrastructure participation. The country’s engineering ecosystem allows it to capture value from global compute expansion without directly competing against dominant American or Chinese AI platforms. In that sense, India’s industrial ecosystem is becoming increasingly aligned with the infrastructure requirements underpinning global AI expansion.

The Real AI Kings May Not Be Software Companies

The emerging economics of AI raise an uncomfortable question for traditional technology narratives. What if the long-term winners are not necessarily the companies building the smartest models, but the firms monetising the energy intensity required to operate them?

The answer increasingly shapes infrastructure investment worldwide. Data centres are evolving into power-hungry industrial assets with operational demands resembling utility infrastructure more than conventional office real estate. AI computing density continues to rise. Cooling complexity continues to increase. Grid stress continues to deepen. Every one of those pressures expands the relevance of industrial suppliers. This does not diminish the importance of software innovation. It changes the hierarchy of value creation around it.

The companies supplying transformers, cooling systems and electrical infrastructure may never dominate headlines the way AI model developers do. They may not attract the same cultural fascination or speculative enthusiasm. Yet their role has become increasingly central to the economics of large-scale AI infrastructure deployment. That is precisely why the sector deserves closer attention. The AI expansion is increasingly driving industrial-scale investment across power, cooling and infrastructure supply chains alongside software development.

India’s Infrastructure Moment May Be Larger Than Markets Realise

The global AI buildout still appears to be in its early stages. Governments, hyperscalers and enterprises continue expanding data centre investments across regions. Power demand forecasts keep rising. Infrastructure bottlenecks remain unresolved. That environment creates sustained demand for the industrial systems supporting compute expansion.

For India, the implications extend beyond individual stock movements. The country’s engineering firms could benefit from rising domestic infrastructure spending as well as growing global investment in AI-related data centre infrastructure. The opportunity sits at the intersection of manufacturing, energy transition and digital expansion. That convergence could reshape how markets define technology leadership.

The next phase of AI-driven investment may extend beyond software platforms and semiconductor development into industrial infrastructure and engineering supply chains. It may increasingly depend on industrial suppliers operating far from the public spotlight. India’s industrial infrastructure suppliers are attracting greater attention as the expansion of AI computing increases demand for power, cooling and engineering systems.