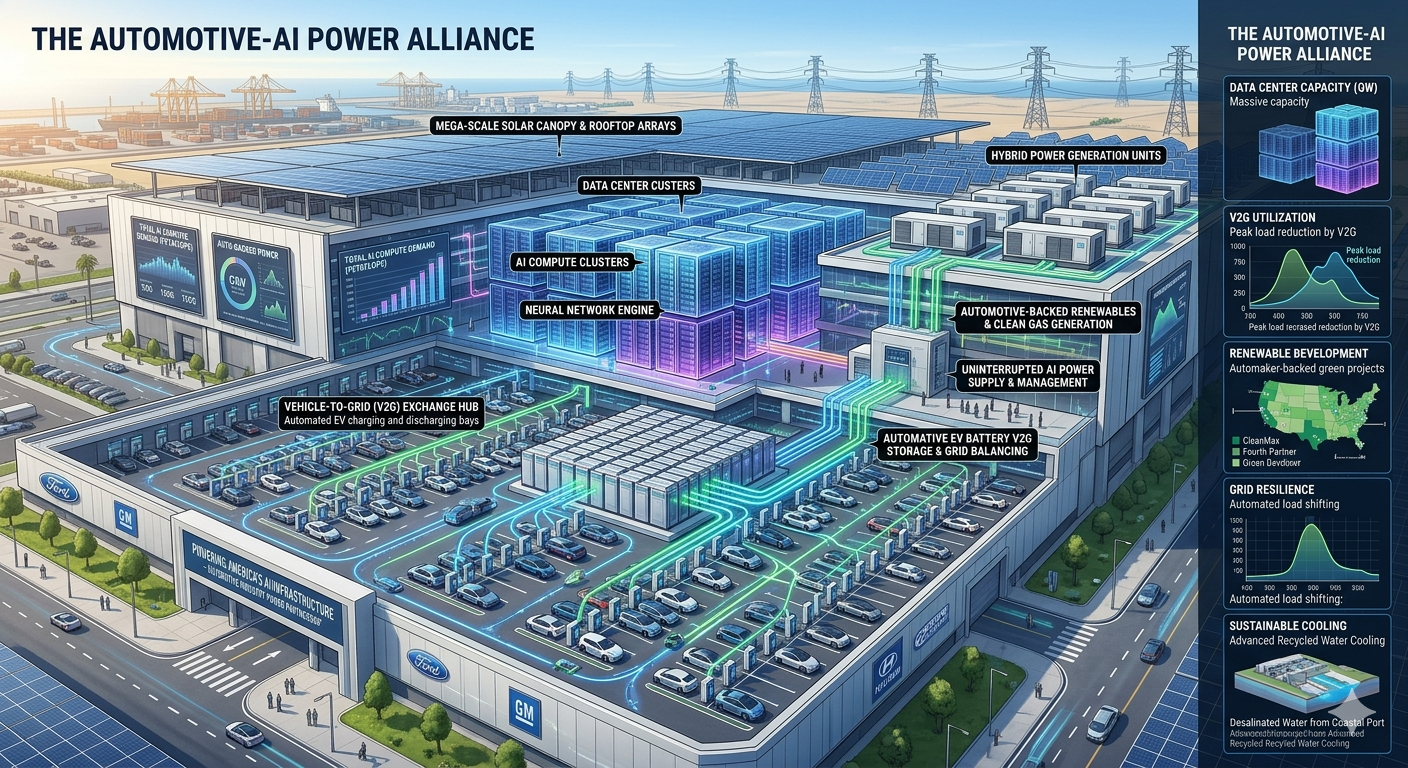

The power crisis gripping AI infrastructure has pulled in an unlikely set of actors: the American automotive industry. As data center operators exhaust conventional paths to grid capacity, a structural realignment is underway in which the battery expertise, manufacturing scale, and stranded EV production capacity of companies like General Motors and Ford are being redirected toward grid-scale energy storage. GM’s announcement on June 9, 2026 which unveiled a sodium-ion battery partnership with startup Peak Energy, an expanded collaboration with battery recycler Redwood Materials, and a near-term lithium iron phosphate supply deal with LG Energy Solution is the most ambitious automaker entry into the energy storage market yet. It is also part of a broader pattern that carries significant implications for AI infrastructure, grid stability, and the long-term economics of stationary storage.

Why Automakers Are Entering the Energy Storage Market

The proximate cause is straightforward: EV battery manufacturing capacity, built at enormous cost and scaled aggressively through 2023 and 2024, is running below utilization as EV demand in the United States has grown more slowly than projected. Ford’s Model e division lost $777 million in the first quarter of 2026 alone, with full-year EV losses projected between $4 billion and $4.5 billion. Rather than mothball the manufacturing infrastructure, both GM and Ford have identified grid-scale battery energy storage systems as a direct commercial application for existing capabilities, supply chains, and engineering expertise.

The demand signal justifying that pivot is unambiguous. The U.S. added a record 15 gigawatts of utility-scale battery storage in 2025, and analysts project approximately 24 GW in 2026 nearly double the prior year. Industry projections call for more than 600 GWh of energy storage on the U.S. grid by 2030. Data centers are a primary driver of that demand. Federal estimates suggest data center power consumption could triple over the next three years, and one projection cited by Electrek places data centers as the source of 83% of all behind-the-meter commercial and industrial storage deployments by 2030. Automakers are not chasing a peripheral opportunity they are entering one of the fastest-growing segments of critical infrastructure at precisely the moment demand is accelerating.

GM’s Three-Layer Strategy

GM’s June 2026 announcement laid out a sequenced approach that addresses both near-term revenue and longer-term strategic positioning in the energy storage market. The first layer is the LG Energy Solution partnership, which extends GM’s existing Ultium joint venture originally established for EV battery production into the grid-scale BESS market. GM will supply lithium iron phosphate cells to LG for integration into its energy storage systems, with production expected to begin within months. This path generates commercial revenue on an immediate timeline, using established chemistry, established manufacturing processes, and an established partner relationship.

The second layer is the Redwood Materials expansion. Redwood already purchases battery scrap from GM’s factories and retired packs from GM’s EV fleet. GM has a pipeline of approximately 10,000 packs directed toward Redwood, and the company has purchased a 7.2 megawatt-hour Redwood second-life system for installation at a GM plant in Michigan an installation GM estimates will generate roughly $3 million in lifetime savings through peak demand shaving and backup power. GM’s Vice President of Battery and Sustainability Kurt Kelty indicated that similar installations across all GM factories are the intended trajectory. The arrangement simultaneously monetizes retired EV batteries, reduces GM’s facility operating costs, and provides Redwood with a large, predictable supply of second-life packs.

The third and most consequential layer is the Peak Energy partnership. GM Ventures has made a strategic investment in Peak Energy, and the two companies are developing an entirely new sodium-ion battery chemistry purpose-built for grid-scale stationary storage. GM will develop the sodium-ion cell at its Wallace Battery Cell Innovation Center in Warren, Michigan retaining exclusive manufacturing rights while Peak Energy integrates the cell into its proprietary passively cooled energy storage platform. First cells are expected to enter trial production in 2028.

Why Sodium-Ion Changes the Cost Equation

The chemistry at the center of GM’s Peak Energy partnership deserves specific attention, because sodium-ion batteries possess a set of characteristics that make them structurally different from lithium-ion for stationary applications.

Sodium is approximately 1,000 times more abundant than lithium and carries significantly lower extraction costs and a reduced environmental footprint. Sodium-ion cells operate across a broader temperature range, exhibit longer cycle life under repeated charge-discharge cycles, and — most significantly for grid-scale deployments carry a materially lower risk of thermal runaway and overheating. That last characteristic is what makes Peak Energy’s passively cooled system architecture possible. The company’s existing storage systems require neither active cooling systems nor fire-suppression infrastructure, both of which add capital cost, operating complexity, and maintenance burden to conventional lithium-iron phosphate installations.

Peak Energy has already deployed what it describes as the world’s first passively cooled grid-scale sodium-ion battery at a site in Colorado. GM’s Paul Menson, director of energy-storage commercialization, summarized the engineering philosophy precisely: the hardest part to engineer is no part at all. Removing the cooling and suppression systems eliminates both upfront cost and ongoing maintenance expense a meaningful advantage in behind-the-meter data center applications where reliability requirements are stringent and operating cost control is a primary concern.

The trade-off is that sodium-ion cells require larger physical footprints to store equivalent energy compared to lithium-ion. For grid-scale stationary deployments at industrial sites or adjacent to data centers, where space constraints are less acute than in vehicle applications, that trade-off is commercially acceptable. Outside of China, no other automaker has announced plans to manufacture sodium-ion cells at commercial scale.

The Redwood-Crusoe Model: Second-Life Batteries Proven at Scale

Before GM’s announcement, Redwood Materials had already demonstrated that second-life EV batteries can deliver reliable, commercial-grade energy storage for AI data centers. In June 2025, Redwood and AI infrastructure company Crusoe commissioned the world’s largest second-life battery microgrid at Redwood’s 100-acre campus in Sparks, Nevada. The system combined 12 megawatts of on-site solar generation with 63 megawatt-hours of energy storage built entirely from repurposed EV battery packs operating fully off-grid and powering four Crusoe Spark modular data centers equipped with NVIDIA A100 and B200 GPUs.

The system recorded 99.2% operational availability over seven months of continuous operation. In March 2026, Crusoe and Redwood announced an expansion from four to 24 Crusoe Spark units at the same site, bringing total compute capacity to nearly seven times the original deployment and power demand to 20 MW. The project’s modular structure allowed that expansion to occur in months rather than the year-plus construction timelines associated with conventional grid-connected data center development.

Redwood currently processes 20 GWh of batteries annually equivalent to approximately 250,000 EVs representing roughly 90% of all lithium-ion batteries recycled in North America. Many of those packs retain 70% to 80% of their original capacity when retired from vehicle use, making them commercially viable for stationary applications where energy density requirements are less demanding than vehicular deployment. Fast Company noted that second-life battery systems can be procured at effectively half the cost of new battery storage a cost advantage that directly addresses the capital intensity of behind-the-meter data center power infrastructure.

Ford’s Parallel Bet

GM’s entry follows Ford, which has made a parallel and equally significant commitment. Ford launched Ford Energy as a wholly owned subsidiary in May 2026, formally converting its Kentucky EV battery gigafactory into a grid-scale BESS manufacturing operation. The division plans to produce 20 GWh of energy storage systems annually, with first customer deliveries targeted for 2028. Ford has committed $2 billion to scale the new business.

On May 18, 2026, Ford Energy and EDF Power Solutions North America signed a five-year framework agreement under which EDF can procure up to 4 GWh of Ford’s DC Block battery storage systems annually, a total potential volume of 20 GWh over the agreement’s term. The DC Block is a standardized 20-foot containerized system built around 512 Ah LFP prismatic cells, offered in two-hour and four-hour discharge configurations. Ford Energy President Lisa Drake’s characterization of the product as “not simply hardware” but rather a long-term operational commitment to grid operators who cannot afford supply chain uncertainty signals that Ford is positioning the division as an industrial-grade infrastructure supplier, not a consumer electronics manufacturer pivoting opportunistically.

What This Means for AI Infrastructure Decision-Makers

For data center operators, enterprise IT leaders, and infrastructure investors, the automaker entry into grid-scale storage introduces a set of commercially meaningful changes worth tracking. First, domestic supply of battery storage systems is expanding materially. Ford Energy and GM’s partnerships with LG and Peak Energy represent new, U.S.-based manufacturing capacity entering a market where supply constraints have historically limited deployment speed. For operators building behind-the-meter storage configurations, broader supplier choice reduces both cost and procurement risk.

Second, second-life battery systems validated at production scale by Redwood and Crusoe are now a credible procurement option for data center storage applications, particularly for peak shaving, demand response, and backup power configurations at industrial density. The 99.2% availability figure from the Sparks, Nevada deployment is the kind of operational data that supports inclusion in enterprise infrastructure specifications.

Third, sodium-ion storage while commercially available only at pilot scale today is tracking toward meaningful market availability in the 2028 to 2030 window. For projects in the planning phase targeting that delivery horizon, the cost and safety profile of sodium-ion, combined with GM’s manufacturing scale and exclusive cell rights, represents a procurement option worth including in long-range power strategy conversations. The AI infrastructure power problem did not originate in Detroit. The solutions increasingly will.